Top 10 Most Common Errors in Damages Calculations – #1: Failure to Consider Saved Expenses

22 July, 2015

22 July, 2015 Ephraim Stulberg

Ephraim Stulberg Canada

Canada

Towards the end of the Great War (or World War I as it came to be called), the American president, Woodrow Wilson, proclaimed Fourteen Points outlining his goals for the reconstitution of Europe, and the international state system as a whole, following the war. The French prime minister at the time, Georges Clemenceau, is purported to have remarked of the self-important American that even “Le bon Dieu n’en avait que dix!”.* For whatever reason, Top 14 lists have never really caught on; Top 10 lists remain en vogue. So, over the next little while, I will be posting on the Top 10 most common errors in damages calculations.

*Clemenceau failed to note, of course, that the Ten Commandments themselves actually contain more than ten commandments**. (Sorry, I am an accountant).

**Now, in fairness, the Hebrew Bible actually does not use the term “Ten Commandments” at all.

By far the most common error I encounter, especially from claims prepared by non-experts but also in occasional decisions of trial judges [1], is the failure to deduct saved expenses. People are generally well aware of their loss of revenue; they are generally less conscious of the fact that the event that caused them to lose revenue has also caused them to save certain expenses. The fact is, almost all situations involving a loss of revenue will also involve a savings in expenses.

All lost profit analyses can be expressed in the following equation. It is so fundamental that I have shown it in a red box:

![]()

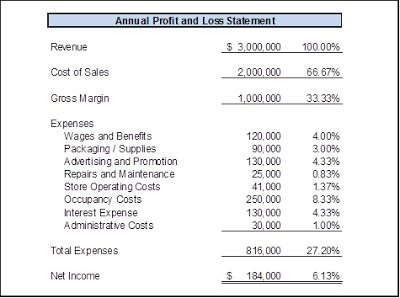

Now, not everyone thinks in terms of red boxes; I, for one, prefer examples. So consider a simple example of a retail store that is forced to close by flooding originating from a neighbouring property. The store’s annual financial statements for the year preceding the flood are as follows:

The closure results in a loss of revenue. But it will save some expenses.

The store will certainly experience a savings in variable costs. Variable costs are costs that – you guessed it – vary in proportion to the level of business activity. For example, to make a sale, the store must give the purchaser the item he or she purchased; it incurs a “cost of sales”. This cost, in our example, has historically been equal to 2/3rds (or 66.66%) of revenue.

The store will also likely experience a savings in its fixed costs. Fixed costs are those that do not vary directly with small fluctuations in business activity, but which are affected by large changes in the business, such as a prolonged shutdown. In the case of our store, if the store is closed long enough the lease may contain a clause relieving the business from paying rent while it is closed; the store may lay off its staff. If the business closes permanently, the annual loss of profit may simply be the difference between the normal revenue and the normal expenses, which in the example of our store is $184,000.

This is, of course, a very schematized example. Calculating saved expenses can be very challenging in practice, in particular when the projected revenue levels contemplate significant growth (or contraction). I will discuss this issue more in future posts, but for now I leave you with this basic lesson:

Lesson: When a business experiences a loss of revenue, it will almost always also experience a savings in expenses. This savings must be offset against the revenue loss to arrive at a proper assessment of lost profits.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

For example, see 1397868 Ontario Ltd. v. Nordic Gaming Corporation (Fort ErieRace Track), 2010 ONCA 101, where the failure to deduct saved expenses resulted in the Ontario Court of Appeal ordering a new trial. It noted that:

[34] I appreciate that the trial judge was confronted with a difficult task in assessing damages in this case. However, her reasons explain how she came to the damages award and it is apparent that she did not account for the cost of sales. Clearly, the cost of sales is an integral part of any loss of profits calculation. Importantly, a deduction for the cost of sales could have a significant impact on the calculation of 139’s loss of profits. In oral argument on appeal, 139’s counsel indicated that if 40 percent of revenues is used to calculate the cost of sales it would “decimate” the damages award. Whatever the case, the failure to deduct the cost of sales could be significant.

Ephraim Stulberg

B.A, M.A, M.BA, CPA, CA, CBV, CFF, Partner/Senior Vice President

- +1 416.366.4968

- estulberg@mdd.com

- Toronto, ON, Canada

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

Renewable Energy Losses – Winds of Change

It is May 20, 1899. New York City taxicab driver Jacob German is the recipient of the United States’ first-ever speeding ticket. He whizzed by at 12 miles per hour on Lexington Avenue and was then pursued and remanded by...

Benefits of Hindsight when Quantifying Financial Losses

Claims for economic losses arising out of failed real estate developments can be complex to prove, requiring evidence concerning many different aspects of the proposed construction project. There can also be different approaches to quantifying losses. Both of these issues...

Waste to Energy

What is Waste to Energy? Waste to energy refers to the process of converting municipal solid waste (MSW), otherwise known as trash, into usable heat, electricity, or fuel. The three main MSW categories include: Biomass or biogenic (plant or animal...

Lost Profits Measurement in the Cannabis Industry

What used to be considered an illicit drug in most countries is now a decriminalized plant with some medicinal potential. Cannabis is in the midst of a global transformation into a major industry with massive investment and growth potential. Canada...

The Varying Effects of a La Niña Cycle on Business Interruption Claims

Earlier this month, Australia’s Bureau of Meteorology announced that the current La Niña conditions would likely continue over the coming months.[i] According to the National Oceanic and Atmospheric Administration, the La Niña effect occurs when there are “periods of below-average...

Business Interruption Measurement Considerations in a COVID-19 World

Although hurricane season doesn’t normally conclude until November 30th, we have already exhausted the modern English alphabet in terms of named hurricanes. In the last year, we’ve also seen an ever increasing number of wildfires, explosions and tropical storms. While...

Claim Considerations Related to the Beirut Port Explosion – Part 2

On 17 October 2019 large numbers of protesters began appearing in Martyrs Square, Nejmeh Square, and Hamra Street, as well as many other areas of Beirut and throughout Lebanon. The reasons for the protests are wide reaching from a social,...

Claim Considerations Related to the Beirut Port Explosion – Part 1

In this two-part series, we write about the claim considerations related to the Beirut port explosion on 4 August 2020. On 4 August 2020 at approximately 18:00 local time, an explosion measuring 3.3 on the Richter scale ripped through Beirut...

How to Calculate Losses Under Business Interruption Coverage

In this article we provide a brief overview of how to calculate losses under business interruption coverage. Broadly speaking, business interruption (“BI”) insurance coverage is meant to indemnify the insured for the loss of profit it suffers as a result...

Forensic Accounting Liability Exposures

The below article first appeared in THE STANDARD, New England’s Insurance Magazine. It features excerpts from a presentation given by MDD partners Paul McGowan, CPA, CVA and Jon Ducey, CPA, CVA on the topic of liability claims and other key...

Economic Damages from Personal Injury: A Forensic Accountant’s Perspective

Regrettably, individuals can experience a temporary or permanent diminishment in their ability to perform certain functions due to a tortfeasor. Forensic accountants and economists are regularly retained in matters involving the injury or death of an individual for the purpose...

Caribbean ‘vacation’ for CAT claims

As a global forensic accounting firm, we at MDD have a “boots on the ground” mentality when it comes to quantifying economic damages for catastrophe (“CAT”) claims. The busy hurricane season in 2017 meant that I, along with many of...

Mining Claim – All Is Not As It Appears

In this briefing we focus on mining claims, and share our knowledge and technical expertise on one of the loss measurement issues regularly encountered in mining claims, production bottlenecks. What you will learn from reading the article include: How the...

Identifying and Measuring Short Duration Business Interruption Losses

What have we really lost? One of the most common issues that arise from short-duration interruptions, those measured in days as opposed to weeks or months, is whether the business actually suffered a permanent loss of revenue or whether the...

Cyclone Debbie May Create Complex Claims Issues for Insurers

Cyclone Debbie and the subsequent rain and flooding events across Queensland, Northern NSW and New Zealand have caused significant damage to property and infrastructure, limited rail access, closed ports and caused damage to numerous roads and bridges. Rail closures in...

Contaminated Products Insurance Claims: How to Check the Costs of a Product Recall

The number of food product recalls reported in the UK through the FSA (Food Standards Agency) rose 78% in 2015. With many UK businesses operating internationally, a product recall situation can impact many countries and cost millions of pounds in...

Staying Afloat in the Flood – The Cost of Flooding to Companies with Exposures in India

Given the number of major flood occurrences in India in the past decade, European and US companies with exposures in the country should examine their insurance coverage and disaster management planning. As the waters start to subside following India’s latest...

The Effect of Deductibles & Policy Wording – Is It What You Think?

With a typical Energy claim standing at approximately USD 4.5 million, it’s no surprise that Business Interruption (BI) is once again the #1 business risk for the fourth year in a row[i]. To help insurers mitigate their exposure when an...

Business Interruption: Complex Interdependencies

As business structures become more complex, companies often need more sophisticated insurance products to properly manage their business interruption risks. For example, narrow vertical integration makes risk management more difficult and increases the demands placed on insurers regarding correct risk...

or Advance Loss of Profit (ALOP) Insurance Cover")

Stemming the Spiralling Cost of Delay: Delay in Start Up (DSU) or Advance Loss of Profit (ALOP) Insurance Cover

Delay in Start Up (DSU) or Advance Loss of Profit (ALOP) insurance cover is an absolute necessity for large and/or complex construction or engineering projects, particularly those financed with structured debt. This insurance was designed to provide cover for the...

Catastrophe Events and Business Interruption Insurance

In the event of a devastating catastrophe (“cat”) be it an earthquake, hurricane, flood, or tornado, the first and foremost priority is to ensure the safety all the people involved. Once this has been established, business owners can then begin...

A Primer To Accurately Calculating Lost Profits

What Are Lost Profits and How Are They Calculated? Lost profits are economic damages caused by a disruption in business operations. The damages can be the result of a variety of factors, some of which include patent infringement, breach of...

I Lost My Customers and It’s Your Fault!

In Schwartz Levitsky Feldman LLP v. Werbin, 2015, an action was put forward by Schwartz Levitsky Feldman (SLF) claiming loss of profits due to the departure of Mr. Werbin. The firm contended that they purchased Werbin’s clients when they purchased...

Foreign Exchange Issues in Damage Quantification: Part II – Applying the Concepts

In the previous post, we presented a basic framework for analyzing the impact of foreign exchange fluctuations on quantifying financial remedies. We argued that the treatment of foreign exchange should be consistent with the principal underlying the financial remedy being awarded;...

Foreign Exchange Issues in Damage Quantification: Part I – Basic Concepts

International trade is an increasingly important part of the Canadian economy, as this picture clearly shows: As a result, it is not uncommon for litigation to involve the quantification of financial remedies across multiple political and monetary boundaries. How does...

Adding up the Damage: Lost Profits vs. Business Value

When a business is destroyed as a result of wrongdoing, there are two commonly used methods by which the plaintiff’s damages may be measured. One method is to appraise the value of the plaintiff’s business at the date of loss;...

Court Breaks with Apportionment

The case of Varco Canada Limited v. Pason Systems Corp., 2013 FC 750 (CanLII) involved an award of over $52M based on an accounting of the defendant’s profits. Perhaps more importantly, the decision sheds light on a number of conceptual...

Calculated Risk: A $75M Award Adds Urgency to Pre-Judgment Interest Considerations

Pre-judgment interest is often the last thing litigants ponder. A recent award of $75 million in pre-judgment interest in Eli Lilly v. Apotex, 2014 FC 1254 (“Cefaclor”) may change that. Cefaclor involved the infringement of patents for an antibiotic. Damages...

Top 10 Most Common Errors in Damage Quantification – #2: “Build It and He Will Come”

I have already written, in another context, about the interaction between physical assets and lost profits. I want to explore the issue from a couple of additional angles. In the 1989 film Field of Dreams, Kevin Costner’s character hears a voice telling him...

Pre-Judgment Interest, Part III: Property Damage, Profit, and PJI

My practice involves a lot of work for property insurance companies. When damage to property occurs, the property owner may advance a claim against the third party tortfeasor for both the value of the damaged property as well as an...

Pre-Judgment Interest, Part II – Interest and Taxes

In the previous post, I discussed the large pre-judgment interest award in Cefaclor. In that case, one of the issues raised by defendant’s counsel was that to award the plaintiff compound interest would result in overpayment; since the damages award is...

Pre-Judgment Interest: Part I: Establishing a Rate – A Basic Framework

This post on pre-judgment interest deals with the basic question: what is the best method by which to calculate a pre-judgment interest rate? The Law Pre-judgment interest is interest that is added to a plaintiff’s monetary award in respect of...

Pre-Judgment Interest: Introduction

Pre-judgment interest is possibly the least sexy topic imaginable. But there is perhaps no better vehicle for a discussion of the fundamental issues involved in financial loss quantification. A short article of mine dealing with a very large PJI award (over...

Top 10 Most Common Errors in Damages Calculations – #1: Failure to Consider Saved Expenses

Towards the end of the Great War (or World War I as it came to be called), the American president, Woodrow Wilson, proclaimed Fourteen Points outlining his goals for the reconstitution of Europe, and the international state system as a...

Tax Rates, Timing and Damages

In Canada, as a general rule, damages awards are subject to the same tax treatment as the monetary amounts they are meant to replace. For example, awards for lost profits are taxed as business income [1]. Litigation can often take...

Dunkin’ Donuts c. Bertico inc., Part II: Lost Profit & Loss of Business Value

Towards the end of its decision in Dunkin’ Brands Canada Ltd. c. Bertico inc.2015 QCCA 624, the Quebec Court of Appeal discussed the issue of whether an award for both a) lost profits up to 2005 and b) loss of business...

Dunkin’ Donuts c. Berticoinc, Part I: The Benchmark Approach to Lost Profits

In April 2015, the Quebec Court of Appeal released its decision in Dunkin’ Brands Canada Ltd. c. Bertico inc. 2015 QCCA 624. The Court of Appeal upheld the trial judge’s ruling (Bertico inc. c. Dunkin' Brands Canada Ltd., 2012 QCCS 2809) that...

Cyber Loss – The Cyber Threat Facing Businesses

Businesses face the risk of financial loss and disruption due to theft of private or sensitive information, attacks on IT systems, and fraud. MDD's Norman Kwan shares that cyber risks policies are still evolving and there are issues that need considerations...

Agricultural Loss – Quantifying Economic Damage for a Hog Farm

Damage quantification for livestock losses can be difficult as it often requires consideration of market price fluctuations, age and weight of livestock at the time of loss and the end purpose of the livestock - considering whether they are for...

Business Interruption Loss – The Interaction between Inventory Losses and Business Interruption Claims

This article explores the areas of overlap between insurance coverage for inventory loss and business interruption. In the event of physical damage to inventory, different policies provide different valuations, including: replacement cost, actual cash value, historical cost or selling price. ...

A New Take on the Accounting of Profits Remedy

The Federal Court’s decision in Merck & Co. v. Apotex Inc. [2013] F.C.J. No. 840, has shed a novel light on to how damages for patent infringement are to be calculated. Previously, in its decision in Monsanto Canada Inc. v....

Quantifying Business Loss Involving Expropriation of Newly Established Businesses

With increasing activity in public works projects in the Greater Toronto Area (e.g. the Toronto-York Spadina Subway extension) and other highway expansions across Ontario, we can expect a large number of businesses to be affected by expropriation. This article will...

Documentation and Litigation

Litigation can be a scary and intimidating process. Preparation is key and includes ensuring that the documentation you need to prove your case is ready at hand. Below are some common forms of litigation and the documentation that should be...

The Global Economy’s Impact on Business Interruption & Extra Expense Claims

While the signs have been around for some time now, the economic crisis that seemed to officially begin with the failure of the U.S. mortgage institutions Fannie Mae and Freddie Mac has now morphed into an unpleasant reality that is...

Coinsurance: Can Someone Please Explain This to me Once And For All?

In the US property insurance market, coinsurance, an often-misunderstood concept, refers to the sharing of risk between the insured and the insurer and applies to property damage and business income loss coverage. Coinsurance as it applies to Property Insurance Because...

Handling Large Complex Claims

Large insurance claims are almost always complex, time-consuming and in need of a forensic accountant. They are complex because of the secondary impact from the misfortune setting off the initial claim. Take, for example, a fire at a ski hill...

Projecting Sales in Business Income Losses is an Art – Not Necessarily a Science

Insurance policies generally state that in determining the Actual Loss Sustained under business income coverage, consideration must be given to actual experience of the business before and the probable experience thereafter had no loss occurred. Thus, the goal in evaluating...

The Impact of Foreign Exchange Rate Movements on Loss of Profit Claims

Foreign exchange risk has been high on the agenda of CFOs of MNCs for many years. With the expansion of the global economy and diverse influences on exchange rates - such as the current climate of economic uncertainty and fear...