Measuring Business Interruption Dependency Claims: A Case Study from Cyclone Gabrielle

22 August, 2024

22 August, 2024-

APAC

APAC

Cyclone Gabrielle made history as the costliest tropical cyclone in the southern hemisphere.

Conceived as a tropical low North of Fiji in early February 2023, Cyclone Gabrielle intensified to as high as Category 3 storm. After downgrading to ex-tropical cyclone status on 12 February 2023, Gabrielle reached the Northern regions of New Zealand’s North Island by 13 February 2023. Gabrielle continued Southeast thereafter, reaching the Eastern coast of the North Island by 14 February 2023.

Over the course of 12 February to 14 February 2023, the northern and eastern regions of the North Island sustained the most severe flooding, damage, and loss of life as a result of the Cyclone with isolated areas in the Coromandel, Hawkes Bay, and Gisborne regions recording more than 400 mm of rain.

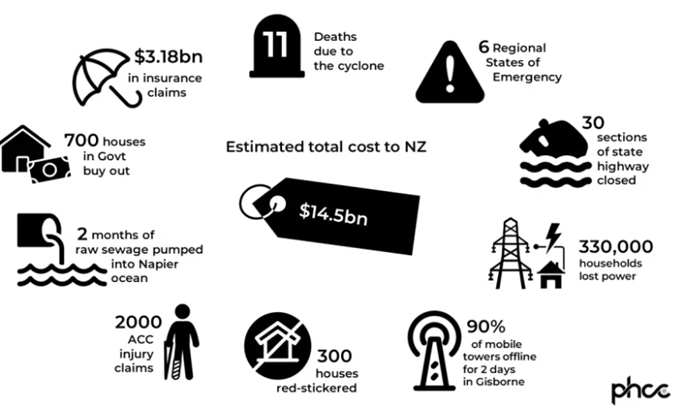

The extensive damage to communities and infrastructure across the North Island prompted New Zealand to declare a national state of emergency for only the third time in its history on 14 February 2023.

The year prior to Cyclone Gabrielle, most regions on the North Island measured record-breaking rainfall through 2022, which was driven by more frequent weather systems during a La Nina periodic season.

The month prior to Cyclone Gabrielle, rainfall approximately 8.5 times greater than the national average was recorded during January 2023. Auckland, New Zealand’s most populated region, saw its wettest January since records began and experienced an extreme rainfall event known as the ‘Auckland Floods’.

This exacerbated flooding on the North Island, with already sodden ground and swollen rivers. A number of rivers burst their stopbanks, releasing torrents of floodwaters across the Hawkes Bay region, in particular, and depositing silt over horticulture and agriculture farmlands.

Cyclone Gabrielle set a world record for the largest number of landslides from one event with approximately 850,000 landslides nationwide.

Impact

Aside from physical damage to property, the Northland, Coromandel, Gisborne, and Hawkes Bay areas, in particular, suffered significant landslips and flooding, which forced the closure of critical road and rail transport routes and shipping ports in and out of these regions.

Alongside transport routes, approximately 332,000 households lost power during the cyclone. While most affected residents had their power restored within a few days, some were without power for more than two weeks.

Power outages across New Zealand led to loss of telecommunications coverage and left eftpos systems offline even after power was restored. Waste, mains, and stormwater utilities were also impacted to varying extents, typically where substations had sustained flood damage. Disruptions were prolonged in areas where significant transport route damage hindered repair crews’ access and in isolated and rural communities.

Data on housing damage classifications following cyclone impacts in 2023 – MBIE 11 January 2023

Insurance Coverage

Whilst the widespread damage caused by flooding, landslides, and silt depository impacted a significant number of communities, many businesses sustained no physical damage. Instead, they were impacted by loss of utilities, prevention of access, closure of key transport routes and ports, or all of the above.

In the absence of physical damage to Insured property, ordinary Business Interruption insurance will not respond to claimants seeking reparation for Loss of Gross Profit, Increased Cost of Working or Extra Expenses.

Many businesses, however, had Dependency or Contingency Coverage Extensions to cover their dependency on customers and suppliers, power, water, and waste utilities, as well as transport routes and ports. This presented businesses who did not sustain physical damage an opportunity to claim for Business Interruption losses directly caused by these contingent perils.

Contingent Business Interruption

Despite dependency extensions coming into effect in response to Cyclone Gabrielle, this coverage came with limitations such as time deductibles, proximity restrictions, and Sub Limit constraints.

These conditions of contingent Business Interruption, however, are nothing new to the New Zealand insurance market.

With a population density of approximately 19.53 people per square kilometre in 2023, New Zealand’s insurance market has been moulded by previous catastrophes and events, and exposure adjusted to reflect the inherently high risk of insuring isolated businesses and communities in New Zealand.

That being said, and despite its prevalence in the market prior to Gabrielle, Dependency Coverage had simply not been tested on a large scale by North Island businesses in recent times, and many businesses may not have considered these limitations in the greater context of their available Business Interruption cover because of this.

Aside from some isolated storm events which are common to the Nelson and West Coast regions of the South Island, the majority of North Island had not seen a severe weather event arguably for decades.

The common challenges in measuring losses under this cover are unpieced further below:

Time Deductibles

Time deductibles, usually between 24 and 72 hours, were often conditional to indemnification under Dependency Extensions. Losses sustained in excess of the time deductible were eligible for cover. In some cases, the time deductible, once exceeded, was also claimable.

As a result of this limitation, many claimants in less severely impacted regions such as Auckland and Coromandel achieved limited coverage periods or were unable to achieve claim acceptance with most utilities restored within time deductible periods.

With at least four North Island regions sustaining widespread damage to utilities infrastructure simultaneously, service providers’ resources were however stretched to remedy utilities damage all at once. Coupled with limited road access, in many causes this resulted in utility outages exceeding 48 hours. This was the case in isolated and rural areas of Northland, Auckland, and the Waikato but more prominent across the Gisborne and Hawkes Bay regions.

Transport Route closures comparatively extended much longer, particular SH 2, and SH 5 which remained closed for as much as five weeks. These highways connected the population of Eastern regions of Gisborne and Hawkes Bay to rest of the North Island.

SH 1 remained closed for approximately one to two weeks in Northland and the Coromandel had their critical SH 25A route closed for more than 10 months, though this damage was instigated by the Auckland Floods event before deteriorating following Gabrielle.

Claimants in proximity to these regional areas were able to outlast most time deductibles. Even so, as trade could typically recommence once power was restored and in the absence of physical damage, claimants often sustained less severe losses on an ongoing basis in contrast to the initial time deductible period.

Proximity Restrictions

Proximity restrictions, though less common became pivotal considerations particularly for dependency coverage triggered by prevention of access and the closure of transport routes and ports.

In this scenario, radius mapping of the named insured locations to nearby affected routes were required to validate the acceptance of a claim. Where the impact to transport routes was pervasive across a given route such as with SH 2 and SH 5, claimants were less affected.

Comparatively, due to the elongated landscape of the Coromandel region, claimants in the Northern areas of the Peninsula were affected by proximity restrictions more so than those in the South. This was because most extended closures of transport routes in the Coromandel occurred in the Southern sections of SH 25 and SH 25A. This proved fatal to Claim acceptance despite periods of loss exceeding any applicable time deductible.

Sub Limit Constraints

Under Dependency Coverage, Business Interruption Sub Limits were often constrained as low as 10% of the total Coverage in place.

For claimants who sustained a period of loss in excess of their applicable time deductible; satisfied applicable proximity restrictions; and had some limited ongoing impact – this cover was typically sufficient.

Comparatively, claimants under the same conditions but with extended outages or who were underinsured, their cover was exhausted rapidly and often before the business had recovered in its fullness.

Communication of this risk to claimant parties was critical and at times lost in translation, particularly in the widespread aftermath of Cyclone Gabrielle.

Causation

Identification of the proximate cause of losses stemming from Cyclone Gabrielle became a key issue.

Many businesses succumbed to extended power outages, prevention of access within the vicinity of their insured premises’, port closures, and multiple road closures simultaneously, and these likely all contributed to a sustained loss of profits in most cases.

Identifying the dominant proximate cause of losses became a challenge for Insurers and policyholders alike, and there wasn’t a single solution widely adopted by market participants.

The quality of financial information to substantiate different causes of loss, changing regional economic environment, and the changing combination of multiple causes of loss between regions (insured or uninsured or both) contributed to the absence of a one – size – fits – all approach.

New Zealand has limited passenger train infrastructure outside of Auckland City, with region travel largely restricted to the use of car transport via State Highways. Both tourists and residents rely heavily on State Highway roading infrastructure which in some cases is restricted to a single transport route such as in Hawkes Bay, Gisborne, and Northland regions with minimal to no detour contingencies available.

Most claimants had extensions to cover dependency on utilities, prevention of access, transport routes and ports, and damage to third parties available. Separating the potential uninsured causes of loss, such as loss of attraction and ongoing disruptive weather, became the integral quantification issue.

Further, where multiple insured causes of loss were sustained, the greatest of the differing time deductibles amongst contingent covers often remained applicable. With the most significant losses typically sustained in the first days following Cyclone Gabrielle, in some cases, claiming ongoing Business Interruption losses through multiple other contingent covers extended the time deductible and resultantly reduced the overall net Business Interruption loss.

Conclusion

With Cyclone Gabrielle severely impacting many different North Island regions and the majority of the population situated in these areas, New Zealand’s existing resources to manage the subsequent claims volumes were tested.

The added complexity of dealing with a large volume of dependency claims meant that Insurers had to rely very heavily on their panel of accountants to unravel the often tangled knot of multiple causation and then make sure that the correct policy limits were applied. This often included managing the expectations of the brokers and their clients.

As many of these claims were relatively low in value, efficient ways had to be found to deal with them to ensure that client expectations in both time and value delivery were met.

MDD has considerable expertise in dealing with these types of claims and the complexities that may occur in a time-efficient and cost-effective manner using its combination of local representation and regional and international depth of resources.

By Josh Herbert and David Maritz.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

MDD LA Wildfires Report

California Wildfires of January 2025: A Devastating Start to the Year The year 2025 began with a series of devastating wildfires that swept through Southern California, leaving a trail of destruction and significant insured losses in their wake. Fuelled by...

CAT Spotlight – Iceland

In this CAT spotlight, we focus on Iceland, situated on the Mid-Atlantic Ridge, a country prone to volcanic eruptions, earthquakes, and glacial floods. The most well-known CAT event in recent times was the March 2010 Eyjafjallajökull eruption. Most will remember...

Recapping the 2024 Hurricane Season

Whilst to most, 01 December marks the countdown towards the festive season, to others on the other side of the Atlantic, it also marks the end of the Hurricane Season (officially on 30 November). Initial Forecast vs. Actual Season Forecast Expectations:...

CAT Spotlight – Italy

In this CAT spotlight article, we look at Italy, where floods and earthquakes have caused the most damage over the last two centuries. As an example of the frequency of seismic events, Italy suffered over 16,000 in 2023, according to...

Measuring Business Interruption Dependency Claims: A Case Study from Cyclone Gabrielle

Cyclone Gabrielle made history as the costliest tropical cyclone in the southern hemisphere. Conceived as a tropical low North of Fiji in early February 2023, Cyclone Gabrielle intensified to as high as Category 3 storm. After downgrading to ex-tropical cyclone...

The Bottom Line of Catastrophe: How Catastrophic (CAT) Events are Impacting the Insurance Industry Worldwide

In this new series of spotlight articles, we look at how CATs are affecting different countries all over the world. These are snapshots of various countries CAT history and are designed to give the reader a basic understanding of the...

Floods in the South of Germany in June 2024: Highly Complex Business Interruption Losses

At the beginning of June 2024, unusually high precipitation occurred in large parts of southern Germany. This resulted in flooding and in property damage to residential and commercial properties over a large area. Initial estimates provided by the German insurance...

Predictions for the 2024 Hurricane Season: Implications for the Insurance Industry

“May 2024 (Tortola): it’s currently 30 degrees (Celsius) down there…” I’ve been very fortunate to experience first-hand the beauty of the Caribbean over the past few years, but you could imagine my surprise, when the diving instructor mentioned the above...

El Niño – Weather Phenomenon & Global Disruptor

What is “El Niño”? In normal conditions in the Pacific Ocean, the trade winds blow westerly along the equator, bringing warm water from around South America towards Asia. In a process known as “upwelling”, cold water from the depths of...

CAT Insights – The Increasing Risk and Frequency of Wildfires

Depending on where you are located, you are likely to experience some sort of “weather disaster season,” such as hurricane season, cyclone season, tornado season, earthquake season, or wildfire season. I live in California where we have earthquake season, which...

Natural Catastrophe Insurance Coverage in Asia: An Overview

Natural Catastrophes in Asia In 2021, Asia was the most severely impacted region, experiencing 40.00% of all disaster events, 49.00% of total deaths, 66.00% of the total number of people affected and 18.90% of all natural catastrophe economic losses worldwide...

Property Damage and Derechos

On 29th June 2023, a rare type of storm called a "derecho" swept across the Midwest region of the United States, mostly impacting the states of Missouri, Illinois and Iowa. The derecho began as a rotating supercell thunderstorm that spawned...

The Broader Impact of CAT Events

While every catastrophe (“CAT event”) leaves a wake of destruction in its path, there are times when the financial impact is more widespread than the physical damage would indicate. Consider the following examples: Pandemic – 2020 The impact of COVID-19...

What to Do When Disaster Strikes & You Can’t Access Financial Documents

Swiss Re’s website sigma-explorer.com noted insured losses for 170 natural catastrophes and 105 man-made disasters in 2021 alone.[i] While almost all of these events resulted in property damage and loss of earnings for the affected businesses, some of those entities...

Calculating the Effects of a Natural Disaster

The Allianz Risk Barometer 2022 reported that natural catastrophes are now the third-highest global business risk, while climate change has moved into the sixth position. These rankings represent 25% and 17% increases from last year.[i] Furthermore, the increasing complexity of...

The Varying Effects of a La Niña Cycle on Business Interruption Claims

Earlier this month, Australia’s Bureau of Meteorology announced that the current La Niña conditions would likely continue over the coming months.[i] According to the National Oceanic and Atmospheric Administration, the La Niña effect occurs when there are “periods of below-average...

The Triple Threat: Pandemic, Natural Catastrophe and Business Interruption

Calculating business interruption losses following a natural catastrophe (“CAT”) has always been as much of an art as a science, requiring forensic accountants to use their education, experience and training to resolve the complexities inherently present in quantifying business interruption...

Claim Considerations Related to the Beirut Port Explosion – Part 2

On 17 October 2019 large numbers of protesters began appearing in Martyrs Square, Nejmeh Square, and Hamra Street, as well as many other areas of Beirut and throughout Lebanon. The reasons for the protests are wide reaching from a social,...

Claim Considerations Related to the Beirut Port Explosion – Part 1

In this two-part series, we write about the claim considerations related to the Beirut port explosion on 4 August 2020. On 4 August 2020 at approximately 18:00 local time, an explosion measuring 3.3 on the Richter scale ripped through Beirut...

Is the Perfect Storm Brewing?

Insurers around the globe currently have their attention firmly fixed on addressing the enormity of client claims relating to COVID-19 but is there another dark cloud gathering on the horizon? Recent scientific information includes NOAA issuing their forecast on May...

Caribbean ‘vacation’ for CAT claims

As a global forensic accounting firm, we at MDD have a “boots on the ground” mentality when it comes to quantifying economic damages for catastrophe (“CAT”) claims. The busy hurricane season in 2017 meant that I, along with many of...

Mexican Standoff – Insured Losses in Mexico Following Recent Catastrophes

September 2017 was a brutal month for the people of Mexico, with two earthquakes and a hurricane causing untold misery, multiple deaths and substantial property damage across the country. But if the general view in the global reinsurance market is...

Business Interruption Insurance and Dealing with Natural Catastrophe Events

Late 2017 has witnessed a flurry of catastrophic weather events that has led to widespread devastation. Hurricane Harvey set the ball rolling, with unprecedented rainfall in the southern United States. Irma then destroyed several Caribbean islands, rendering many uninhabitable, before...

Cyclone Debbie May Create Complex Claims Issues for Insurers

Cyclone Debbie and the subsequent rain and flooding events across Queensland, Northern NSW and New Zealand have caused significant damage to property and infrastructure, limited rail access, closed ports and caused damage to numerous roads and bridges. Rail closures in...

Financial Impact of New Zealand Kaikoura Earthquakes Felt Beyond Earthquake Zone

While the damage to physical property as a result of the Kaikoura earthquakes in November 2016 has been well documented, the financial impact of these events are ongoing both on businesses physically affected by the earthquakes as well as businesses...

Staying Afloat in the Flood – The Cost of Flooding to Companies with Exposures in India

Given the number of major flood occurrences in India in the past decade, European and US companies with exposures in the country should examine their insurance coverage and disaster management planning. As the waters start to subside following India’s latest...

Canadian Wildfire Present Challenges to Business Owners and Their Insurers

The Canadian wildfire which started in early May 2016 southwest of Fort McMurray affected a population of about 90,000 and led to destruction of over 2,400 structures. The sheer ferocity and speed of the fire took both public services and...

Catastrophe Events and Business Interruption Insurance

In the event of a devastating catastrophe (“cat”) be it an earthquake, hurricane, flood, or tornado, the first and foremost priority is to ensure the safety all the people involved. Once this has been established, business owners can then begin...

What to do When You Can’t Get to Documents

On June 20, 2013 Southern Alberta endured a catastrophic flood resulting in a significant amount of property damage, numerous civil authority evacuations and power outages for individuals and businesses. In any major catastrophe, access to supporting documentation may not be...

The Forensic Accountant’s Role in a Large Loss

No matter how well a risk management team has planned for it, actually dealing with a catastrophe can be a distracting and stressful financial challenge. The adjuster's ability to manage his resources and work through the complex claim issues that...