Accounting For Attorneys

15 August, 2013

15 August, 2013 USA

USA

It is becoming increasingly important for attorneys to understand financial statements and their relevance to various types of business and legal situations. The non-accountant attorney will greatly benefit from a basic understanding of the key principles of accounting. Equally important is the understanding of forensic accounting and how the forensic accountant can be an asset to the attorney.

What is Accounting?

Accounting is the backbone of business. It is the discipline of measuring, communicating and interpreting financial activity. The end result should produce a financial image of the business that supports the decisions of managers, informs investors of business developments and assists in keeping the business profitable. Accounting is also widely referred to as the “language of business” [1].

What do Accountants do?

A number of disciplines are involved in accounting. A few of the major accounting fields are:

Bookkeeping

At the root of all accounting is bookkeeping, the practice of recording transactions. Bookkeepers tend to focus on the details, recording transactions in an efficient and organized manner, and they may or may not see the overall picture.

Managerial accounting

These accountants typically work for a single company or entity and use the work done by bookkeepers to produce and analyze financial data for the business. An accountant can design reports that will capture all of the details necessary to satisfy the needs of the business – managerial, budgeting, financial reporting, projection, analysis, and tax reporting. These accountants may work among a large staff of accounting personnel and may be a controller or a financial officer of the company.

Public accounting

Many businesses, governmental organizations, non-profit organizations, and individuals use the services of a certified public accountant. (CPA). These accountants provide a wide range of services, including consulting on taxes, accounting, and auditing.

Auditing

An auditor can be either an internal or external auditor.

- An internal auditor typically works for a single entity and is responsible for checking the company’s records to ensure that they are correct and looking for problems such as inefficiency or criminal activities.

- External auditors are certified public accountants who are independent of the entity. An external auditor examines a company’s accounting books and records in order to determine accuracy and whether the company is following appropriate accounting procedures. An auditor issues an opinion in a report that states whether the financial statements present fairly the company’s financial position and its operational results in accordance with Generally Accepted Accounting Principles (GAAP).

Forensic accounting

A forensic accountant applies auditing and accounting concepts and theories to investigate an actual or suspected situation involving actual or potential litigation – in other words, investigative accounting. Forensic accounting typically deals with activities like fraud, embezzlement, legal disputes, insurance claims, money laundering, or bankruptcies. Analyzing and investigating these situations requires an awareness of finance and accounting along with knowledge of the law and investigation skills.

Certifications Held by Accountants

Special designations or certifications that exist for accountants provide additional evidence of knowledge and competence beyond that provided by the college degree. These certifications allow accountants to project to clients the depth of their knowledge in a specialized field within accounting. The following are some of the various certifications available to accountants.

CPA – Certified Public Accountant

CPA is the statutory title of qualified accountants in the United States who have passed the Uniform Certified Public Accountant Examination and have met additional state education and experience requirements for certification as a CPA. In most U.S. states, only CPAs who are licensed are able to provide to the public attestation (including auditing) opinions on financial statements.

CFE – Certified Fraud Examiner

The ACFE (Association of Certified Fraud Examiners) established and administers the CFE designation. This designation denotes proven expertise in fraud prevention, detection, deterrence and investigation. To become a CFE, one must pass a rigorous examination administered by the Association of Certified Fraud Examiners (ACFE), meet specific education and professional requirements, exemplify the highest moral and ethical standards and agree to abide by the CFE Code of Professional Ethics.

CVA – Certified Valuation Analyst

The CVA accreditation is a statement to the business, professional and legal community that an individual has attained a level of knowledge in business valuations that the National Association of Certified Valuators and Analysts (NACVA) considers exemplary and worthy of recognition by awarding the designation of CVA) To become certified by NACVA, the candidate is required to successfully complete a rigorous training and testing process. A pre-emptive requirement to becoming a CVA is that the applicant must be a Certified Public Accountant (CPA) registered in his or her state.

MAFF – Master Analyst in Financial Forensics

The MAFF credential is offered through a subsidiary of NACVA, the Financial Forensics Institute. It is designed to provide assurance to the legal and business communities — the primary users of financial forensics services — the designee possesses a level of experience and knowledge deemed acceptable by the Association to provide competent and professional financial forensic support services. Applicants can train in one of seven areas of speciality, any of which lead to earning one’s MAFF credential. Those areas are: Bankruptcy Insolvency and Restructuring, Economic Damages, Business and Intellectual Property Damages, Business Valuation in Litigation, Forensic Accounting, Fraud Risk Management, and Matrimonial Litigation. Earning the credential requires consideration of all of the person’s qualifications and commitment to the discipline; this includes prior education and experience, prerequisite and required training as provided (or recommended) by NACVA, testing, and post-requisite requirements for recertification.

ABV – Accredited in Business Valuation

Similar to the CVA, the ABV credential is administered by the AICPA and is conferred upon CPAs who have demonstrated the skill, education and experience necessary to satisfy stringent requirements. These requirements were designed to address certain areas of skill, education and experience that are critical to practicing business valuation successfully.

CFA – Chartered Financial Analyst

The CFA is a professional designation given by the CFA Institute that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Before an accountant can become a CFA charter holder, they must have a minimum of three years of investment/financial experience and hold a bachelor’s degree.

CFF – Certified in Financial Forensics

A relatively new forensic credential was launched in the fall of 2008 by the AICPA. The credential combines specialized forensic accounting expertise with the core knowledge and skills that make CPAs among the most trusted business advisers. The CFF encompasses fundamental and specialized forensic accounting skills that CPA practitioners apply in a variety of service areas, including bankruptcy and insolvency, computer forensics, economic damages, family law, fraud investigations, financial statement misrepresentation and valuations.

Accounting Basics

You’ve probably heard the saying, “Money doesn’t grow on trees.” It means that money must come from somewhere—it doesn’t just appear. An accounting system is used to record the source and outflow of money from a business.

Double-entry bookkeeping

This is a method of accounting that lets you track just where your money comes from and where it goes. Using double-entry means that money is never gained or lost—it is always transferred from somewhere (a source account) to somewhere else (a destination account). This transfer is known as a transaction, and each transaction requires at least two accounts. An account is a record for keeping track of what you own, owe, spend or receive. For example, a phone bill is paid from a checking account and money transfers from your bank to the phone company. This is a transaction transferring money from a bank account to a phone expense account. This double-entry concept has been around since the 13th century, and its purpose has always been to reduce the likelihood of data-entry errors. In a double-entry transaction, an equal amount is always transferred from one account (or group of accounts) to another account (or group of accounts), keeping the books in balance.

Debits & Credits

Accountants use the terms debit and credit to describe whether an account is increased or decreased. Debits and credits are a system of notation developed before a concept of positive and negative numbers were in use. If a certain type of account normally has a debit balance, a credit balance is a way of denoting a negative quantity of that item. For example, your bank account is an asset and normally has a debit balance. If that account in your books has a credit balance, you owe the bank money (you’re overdrawn). Nobody inventing double-entry bookkeeping today would use left-and-right debits and credits–he or she would certainly use positive and negative numbers, which is exactly what almost all computer programs do that perform bookkeeping. It would be better to think of double-entry bookkeeping as a system (in the abstract sense of the word) in which the “entity” begins with nothing, and every change in assets (a debit to increase, a credit to decrease) has an equal and opposite reaction.

Source Documents

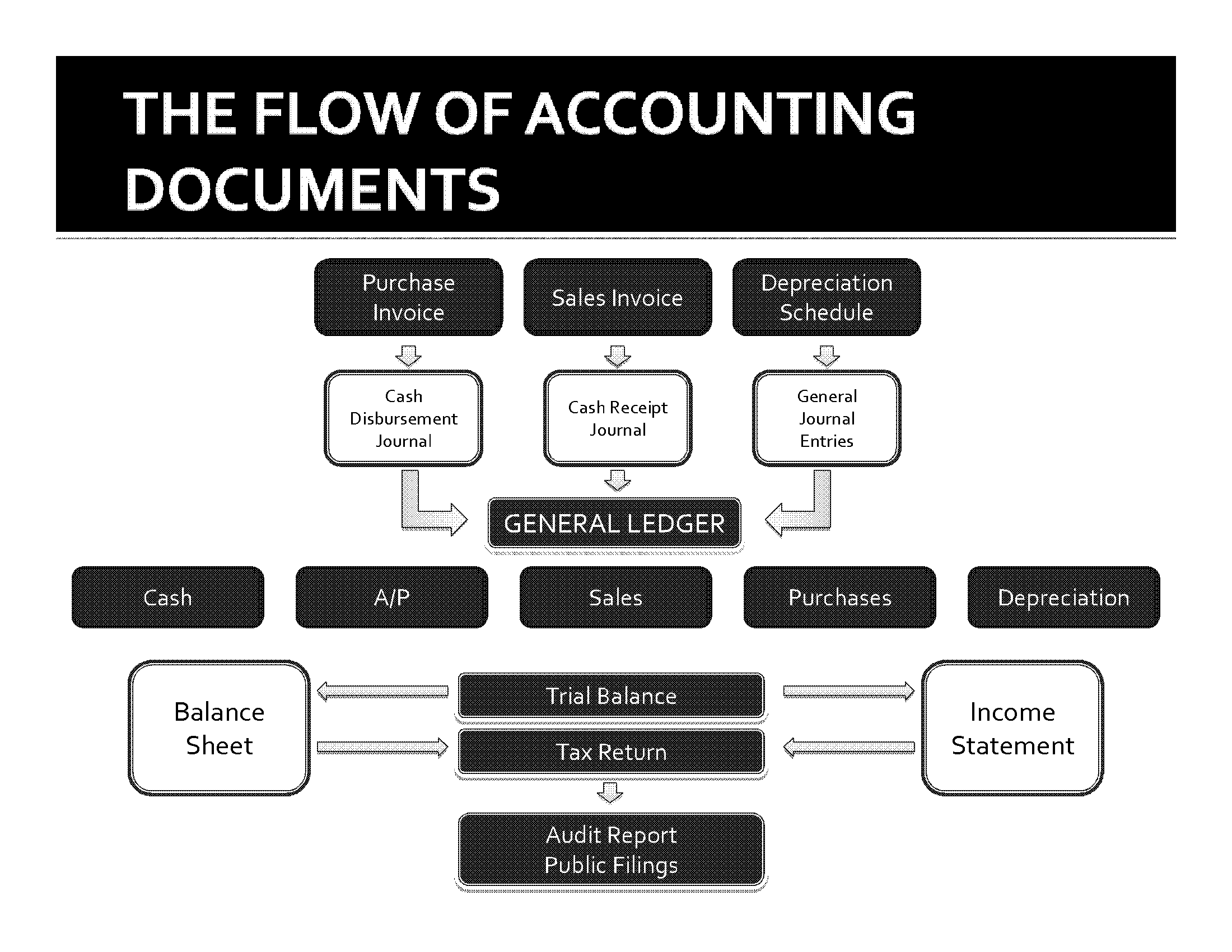

In the normal course of business, a document is produced each time a transaction occurs. Sales and purchases usually have invoices or receipts. Deposit slips are produced when deposits are made to a bank account. Checks are written to pay money out of the account. Bookkeeping involves recording the details of all of these source documents into multi-column journals. A simple diagram illustrating the flow of accounting documents is presented below and shows the progression from the source documents to journals to the general ledger accounts and to the resulting financial reports.

The Financial Statements

Financial statements are usually comprised of three separate statements: the Balance Sheet, the Income Statement (Profit and Loss Statement) and the Statement of Cash Flows. In addition to the basic financial statements, some financials will include Notes to the Financial Statements. Be sure to review this information for contingent liabilities and other important information.Financials statements can be compiled many different ways. The primary methodologies are cash basis, accrual basis and tax basis accounting.

- Cash basis accounting essentially reports revenues and expenses only when the cash is received or paid; whereas, accrual basis accounting reports revenues when they are earned and expenses when they are incurred.

- Accrual basis accounting attempts to match the revenues received with the expenses incurred and record them in the same accounting period regardless as to when the cash changes hands.

- Tax basis accounting reports revenues and expenses in accordance with the Internal Revenue Code (IRC). Tax basis financials should also identify if they are prepared on the cash or accrual basis of accounting.

Balance Sheet

The Balance Sheet has three sections: assets, liabilities, and equity. Assets less liabilities will equal equity if you have a proper Balance Sheet.

Assets

An asset is an economic resource that is owned or controlled by an entity; something of perceived value obtained through the exchange of another asset. For example, a law firm provides services to its clients creating an account receivable or cash. Assets are typically presented at cost (the price the company paid for them plus incidental costs). Some assets are presented at market value. Assets on a Balance Sheet are arranged in order of liquidity from greatest to least.

Questions to ponder:

- How liquid are the assets of the company?

- Is there sufficient cash to cover any litigation and settlement costs?

- How is inventory valued by this company?

- What are any “other assets” listed?

- How will this action or lawsuit impact the assets of the company?

- Are there any intangible assets? What are they worth?

- Does the company have a backlog of orders or work to help ensure profitability in the future?

Liabilities

Liabilities represent obligations to pay to lenders and creditors in the future for assets or services provided to the entity by the lenders or creditors in the past.

Questions to ponder:

- Are the debts shown real? Are loans from the owner ever going to be repaid?

- Are there any unrecorded debts (such as unpaid taxes, including payroll or credit card debt)?

- Are there any contingent liabilities (such as debt guarantees, environmental clean up costs, litigation, purchase commitments, etc.)?

- How are leases treated (capitalized or expensed)?

Equity

Equity is the book value of an ownership stake in a company. Equity is not typically representative of the true market value of a company. Rather, further analysis into the company’s assets, liabilities and future earnings capability is required to determine the true market value.Changes in equity typically occur from contributions or distributions of funds by the owners or a profit or loss by the company. Changes can also occur from the restatement of a prior period due to an accounting error.

Income Statement

The Income Statement details the revenue (also known as sales, gross income, or gross receipts) and expenses of an entity for the time period presented. Typically, an Income Statement presents a subtotal for the revenue and expenses from operations and then accounts for “other income and expenses” after the subtotal. These other income and expenses could be gain or loss on the disposal of equipment, incidental interest income from a savings account, etc. Almost every company’s Income Statement will be unique in one way or another, including how transactions are classified within accounts. A thorough understanding of how the company accounts for transactions is necessary. For example, some companies will include the collection of sales tax in gross revenue; others will not. The same goes for freight expenses passed on to the customer. Understanding the motivation for a company’s financial presentation will help you better understand their financials.

Revenue recognition

It is frequently a problem with revenue recognition issues when an accounting scandal comes to light. The increased pressure to meet earnings expectations of shareholders has driven management to manipulate the Income Statement. In privately held companies, the bonus or commission plans are usually the culprits behind manipulated earnings. For example, a sales agent whose primary compensation is based on commission and exceeding quarterly sales objectives will typically push hard towards the end of a quarter to push themselves into the next higher threshold of payouts. This can possibly be accomplished by changing the date of the sale closing or submitting sales that truly are not yet realized.Each reporting entity will have their own rules for revenue recognition. These rules are included in the IRC (Internal Revenue Code) or GAAP (Generally Accepted Accounting Principles), and are similar in some areas. They are complex and too numerous to discuss here.

Cost of goods sold

A company that maintains an inventory must account for the cost of goods sold and this can become a tricky situation. Cost of goods sold is generally calculated by adding the beginning inventory value to purchases during the period and deducting the ending inventory value. There is lots of room for interpretation in the inventory values. There are several accepted methodologies for calculating the inventory values, including: Last-In-First-Out (LIFO), First-In-First-Out (FIFO), and weighted average cost. In an economy of rising prices, a FIFO inventory will typically lead to a higher gross profit and a lower Inventory value on the Balance Sheet as compared to LIFO.

The most important thing to remember when reviewing Income Statements is to ask many questions about the company’s process for recording revenue and expenses, whether there are any related party transactions and what rules of accounting they are following.

Questions to ponder:

- Does the company pay personal expenses of the owner(s)?

- Are the owner(s)’ salaries/bonuses reasonable?

- Does the owner have an auto-mobile or entertainment allowance?

- Is the company’s revenue seasonal from month to month or from year to year? What causes the seasonality?

- Does the cost of goods sold percentage hold fairly steady? If not, why?

Statement of Cash Flows

The inclusion of a Statement of Cash Flows indicates the entity is on the accrual method of accounting. Because accrual accounting attempts to match revenue with expenses, the flow of cash will not typically match the Income Statement. The Statement of Cash Flows is a reconciliation of cash and cash equivalents. The Statement of Cash Flows is broken down into three sections: Operating, Investing and Financing activities. This statement provides additional information that cannot be gleaned from reading the Balance Sheet or Income Statement and is a good source of how the company uses its cash.

Reliability of a Financial Statement

Anyone can put together a financial statement. The quality of a financial statement will reflect the ability of the person who put the statement together. Certified Public Accountants (CPAs) have had formal training in financial statement preparation and have passed exhaustive testing on financial statement knowledge. Most states also have experience requirements for the preparation of financial statements under a more seasoned CPA. In addition, CPA licensure and compliance are regulated by state government bodies. Therefore, a financial statement prepared by a CPA would likely be more reliable than one prepared by a bookkeeper.If a CPA in public practice (as opposed to a Controller or CFO) issues a financial statement, certain reporting requirements reveal the level of assurance the CPA is providing regarding the financials. An “in-house” CPA is not required, or allowed, to issue one of these three reports for third party use.Keep an eye out for a “Going Concern” clause in the accountant’s report or the notes to the financial statements. A “Going Concern” clause indicates that the company is not financially stable and may not be in existence a year from the date of the financials.

Audited by a CPA

An Audit provides the highest level of assurance a CPA can offer for a financial statement. The CPA attaches an audit report to the financial statements with one of four general opinions: Unqualified, Qualified, Disclaimer, or Adverse. An unqualified opinion is the best level of assurance that the financial statements are presented fairly, in all material respects, in accordance with generally accepted accounting principles (GAAP). A qualified opinion means there are some material GAAP departures but they are not so severe as to result in a disclaimer or adverse opinion. A disclaimer of opinion essentially says that the auditor was unable to perform all the necessary procedures of an audit and therefore disclaims any opinion. An adverse opinion occurs when there is a very material departure from GAAP that cannot be reconciled. This type of opinion is rarely issued. An audit is designed to provide “reasonable assurance” that the statements are “free of material misstatement.”To perform an audit, the CPA examines on a “test basis” evidence supporting the amounts and disclosures in the financial statements and evaluates the accounting principles used and any significant estimates made by management.The CPA communicates with a sample of the company’s customers to verify that accounts receivables exist and are properly valued. The CPA observes the physical inventory count to verify that the assets exist and there is no obsolete inventory. Typically, the CPA communicates with all material financial institutions to verify the existence and value of the assets or liabilities and that no other liabilities exist with that institution.An audit does not provide a guarantee of accuracy of the information presented in the financials.

Reviewed by a CPA

A review is when a CPA formally examines a financial statement prepared by management. The accountant asks questions of management to make sure they are following GAAP or other pertinent rules. Also, the financial statements are checked mathematically and for internal consistency to see if the numbers “make sense.” If appropriate, the statements are compared to industry data (analytical review).The accountant is not required to check or test the balances in the accounts. An accountant can sit in a room with a company’s financial statement, the controller of a company and a sheet of industry data and perform a review without leaving the room or contacting any third parties.

Practice tip: Do not ask of a CPA witness “have you reviewed this financial statement?” Review is a term of art to a CPA. Unless they signed a review report they should answer no. They may respond: “I have examined the financial statement;” “I have analyzed the financial statement;” “I have observed many deficiencies in this financial report, but I have not reviewed it.”

Compiled by a CPA

This is where a client furnishes the financial information and requests that the accountant prepare proper financial statements. This can range from simply printing a computerized report (often from a program like QuickBooks) to recommending adjusting entries or taking a box of documents, the check book and credit card statements and creating a financial statement from that information.

Internal Financial Statements

The reliability of internal financials depends on the quality of the company and the quality of the accountant preparing them.

Tax Returns

Tax returns for business entities typically contain the information presented in financial statements in a slightly different format. Also, the amounts may be different because financial statements usually follow GAAP rules whereas tax returns usually follow Internal Revenue Code (IRC) rules.

When obtaining financial statements, determine the original reason for creation of the financials. Within the rules, there is usually room to “skew” the numbers to help present the best financials (for a bank loan) or the worst (for the tax return).

Financial Ratios

Ratios can help decipher a company’s financials and allow you to compare a company to an industry standard. Below are a few of many available ratios that are more useful in the litigation setting to determine if a company is financially stable enough to deal with a lawsuit.

Current Ratio

This ratio provides the user with an indication if the company will be able to pay its bills for the next year.The current Ratio is the number you get when you divide current assets by current liabilities. A one-to-one ratio shows the company will have just enough assets to pay debts.

Working Capital

Working Capital is the amount by which current assets exceed current liabilities. This is the amount of funds that are not committed to existing debts and can be used for new projects.

Acid Test

The acid test reveals how much cash the company can raise quickly. It is calculated by reducing Working Capital by the Inventory value.

Documents and Document Requests

Document requests are going to be specific for each case based upon the circumstances and desired goal. In accounting, the goal is to always be able to trace an amount on a financial statement back to a source document. Accountants love paper. We have listed many of the documents likely to be available in the accounting records of an entity, from the high level summary documents down to the detailed documents for each transaction.Most entities today use an electronic accounting system rather than maintaining a manual system. When requesting a large volume of documents that need to be analyzed, it is recommended that you obtain the information electronically. The electronic formats will vary greatly and your accounting expert may have the resources to open virtually every format, but don’t count on it – ask your expert what they can handle.

Be wary of accounting documents identified as “reports” or “transaction reports,” or the like. Obtain written clarification of what the report is purported to show because many of today’s accounting systems allow you to run numerous filters on reports so only certain transactions are included and shown. But often the report itself does not clearly detail the filters in place. Be sure to identify the time periods you wish to see and the frequency with which you desire to see the statements (i.e. monthly, quarterly, annually).

Documents that may be requested are listed below.

- Balance Sheets

- Income Statements

- Statement of Cash Flows

- Statement of Changes in Financial Position

- Budgets

- Job Cost Reports

- Federal Income Tax Returns

- State Income Tax Returns

- State Sales or Excise Tax Returns

These returns will provide revenue amounts. - Federal and State Payroll Tax Returns

These returns will provide detail of payroll amounts paid by the company and a listing of all the employees and amounts received. - Trial balance

The trial balances lists all of the general ledger account balances as of the date specified with total amounts being either a debit or a credit; used to prepare financials statements and tax returns. - Detailed General Ledger

The general ledger typically lists all the accounts with a beginning balance from the previous period, all the transactions during the specified period and the ending balance for each account. In more sophisticated accounting systems, certain transactions will be posted to the general ledger in batch entries, hiding the detailed transactions. This will result in a need to obtain the subsidiary ledgers. More basic accounting software such as QuickBooks and Peachtree do not have separate subsidiary ledgers. - Subsidiary Ledgers

The subsidiary ledger contains the detailed information for an account. Typically subsidiary ledgers are accounts receivable (A/R), accounts payable (A/P), sales ledger, payroll ledger, etc. - Journals

Accounting systems will typically maintain journals for each transaction. A common journal to be wary of is the General Journal, which is typically where general journal entries are made. General journal entries are an area to scrutinize because this journal bypasses the normal accounting process and enters a transaction directly to the general ledger and represent unusual or non-recurring transactions. Another journal is the sales and purchase journals. - Source Documents

These documents include a sales invoice, a bill or purchase invoice, a purchase order, requisition request, contracts, promissory notes, bank statements, brokerage statements, accounts receivable statements, inventory count sheets, cancelled checks, vehicle licensing documents, business licensing documents, cash register receipts, other cash receipts, articles of incorporation or other formation documents, by-laws, purchase commitments, marketing materials, leasing documents, etc.

Glossary [2]

Capitalized terms that appear within definitions of other terms are also defined in the glossary. Related terms are cross-referenced to provide a clearer understanding of their interdependent relationships.

Account – An accounting record in which the results of transactions are accumulated; shows increases, decreases, and a balance.

Accountant – Person skilled in the recording and reporting of financial transactions. (See CERTIFIED PUBLIC ACCOUNTANT.)

Accountants’ Report – Formal document that communicates an independent accountant’s: (1) expression of limited assurance on FINANCIAL STATEMENTS as a result of performing inquiry and analytic procedures (Review Report); (2) results of procedures performed (Agreed-Upon Procedures Report); (3) non-expression of opinion or any form of assurance on a presentation in the form of financial statements information that is the representation of management (Compilation Report); or (4) an opinion on an assertion made by management in accordance with the Statements on Standards for Attestation Engagements (Attestation Report). An accountants’ report does not result from the performance of an AUDIT. (See AUDITORS’ REPORT)

Accounting – Recording and reporting of financial transactions, including the origination of the transaction, its recognition, processing, and summarization in the FINANCIAL STATEMENTS.

Accrual-Basis Accounting – A system of accounting in which revenues and expenses are recorded as they are earned and incurred, not necessarily when cash is received or paid.

Adverse Opinion – Expression of an opinion in an AUDITORS’ REPORT which states that FINANCIAL STATEMENTS do not fairly present the financial position, results of operations and cash flows in conformity with GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP). The auditor will issue an adverse opinion when there is an existence of a material weakness on the effectiveness of internal control over financial reporting.

American Institute of Certified Public Accountants (AICPA) – National professional membership organization that represents practicing CERTIFIED PUBLIC ACCOUNTANTS (CPAs). The AICPA establishes ethical and auditing standards as well as standards for other services performed by its members. Through committees, it develops guidance for specialized industries. It participates with the Financial Accounting Standards Board (FASB) and the Government Accounting Standards Board (GASB) in establishing accounting principles.

Articles of Incorporation – (sometimes also referred to as the “Certificate of Incorporation” or the “Corporate Charter”) the primary rules governing the management of a corporation in the United States, and are filed with a state or other regulatory agency.

Asset – An economic resource that is expected to be of benefit in the future. Probable future economic benefits obtained as a result of past transactions or events. Anything of value to which the firm has a legal claim. Any owned tangible or intangible object having economic value useful to the owner.

Audit – The result of an independent accountant’s review of the statements and footnotes to ensure compliance with GENERALLY ACCEPTED ACCOUNTING PRINCIPLES and to render an opinion on the fairness of the financial statements.

Auditor – Person who AUDITS financial accounts and records kept by others. Includes both public accounting firms registered with the PCAOB and associated persons thereof.

Auditors’ Report – Written communication issued by an independent CERTIFIED PUBLIC ACCOUNTANT (CPA) describing the character of his or her work and the degree of responsibility taken. An auditors’ report includes a statement that the AUDIT was conducted in accordance with GENERALLY ACCEPTED AUDITING STANDARDS (GAAS), which require that the AUDITOR plan and perform the audit to obtain reasonable assurance about whether the FINANCIAL STATEMENTS are free of material misstatement, as well as a statement that the auditor believes the audit provides a reasonable basis for his or her opinion. (See ACCOUNTANTS’ REPORT.)

Balance Sheet – Basic FINANCIAL STATEMENT, usually accompanied by appropriate DISCLOSURES that describe the basis of ACCOUNTING used in its preparation and presentation of a specified date the entity’s ASSETS, LIABILITIES and the EQUITY of its owners. Also known as a STATEMENT OF FINANCIAL CONDITION.

Board of Directors – Individuals responsible for overseeing the affairs of an entity, including the election of its officers. The board of a CORPORATION that issues stock is elected by stockholders.

Bookkeeping – The recording of all financial transactions undertaken by an individual or organization. A financial transaction is any event that involves money.

Capital Stock – Ownership shares of a CORPORATION authorized by its ARTICLES OF INCORPORATION. The money value assigned to a corporation’s issued shares. The BALANCE SHEET account with the aggregate amount of the PAR VALUE or STATED VALUE of all stock issued by a corporation.

Cash-Basis Accounting – A system of accounting in which transactions are recorded and revenues and expenses are recognized only when cash is received or paid.

Certified Public Accountant (CPA) – ACCOUNTANT who has satisfied the education, experience, and examination requirements of his or her jurisdiction necessary to be certified as a public accountant.

Chief Financial Officer (CFO) – The corporate executive who is responsible for overseeing the financial activities of an entire company. This includes signing checks, monitoring cash flow, and financial planning.

Controller – An employee, often an officer, of a business firm who checks expenditures, finances, etc.; comptroller.

Corporation – Form of doing business pursuant to a charter granted by a state or federal government. Corporations typically are characterized by the issuance of freely transferable CAPITAL STOCK, perpetual life, centralized management, and limitation of owners’ LIABILITY to the amount they invest in the business.

Credit – Entry on the right side of a DOUBLE-ENTRY BOOKKEEPING system that represents the reduction of an ASSET or expense or the addition to a LIABILITY or REVENUE. (See DEBIT.)

Creditor – Party that loans money or other ASSETS to another party.

Debtor – Party owing money or other ASSETS to a CREDITOR

Debit – Entry on the left side of a DOUBLE-ENTRY BOOKKEEPING system that represents the addition of an ASSET or expense or the reduction to a LIABILITY or REVENUE. (See CREDIT.)

Disclosure – Process of divulging accounting information so that the content of FINANCIAL STATEMENTS is understood.

Dividends – Distribution of earnings to owners of a CORPORATION in cash, other ASSETS of the corporation, or the corporation’s CAPITAL STOCK.

Double-Entry Bookkeeping – Method of recording financial transactions in which each transaction is entered in two or more accounts and involves two-way, self-balancing posting. Total DEBITS must equal total CREDITS.

Equity – Residual interest in the ASSETS of an entity that remains after deducting its LIABILITIES. Also, the amount of a business’ total assets less total liabilities. Also, the third section of a BALANCE SHEET, the other two being assets and liabilities.

Expenses – Costs incurred in the normal course of business to generate revenues.

External Auditors – Independent CPAs who are retained by organizations to perform audits of financial statements.

Financial Accounting Standards Board (FASB) – Independent, private, non-governmental authority for the establishment of ACCOUNTING principles in the United States.

Financial Statements – Presentation of financial data including BALANCE SHEETS, INCOME STATEMENTS and STATEMENTS OF CASH FLOW, or any supporting statement that is intended to communicate an entity’s financial position at a point in time and its results of operations for a period then ended.

First in, First out (FIFO) – ACCOUNTING method of valuing INVENTORY under which the costs of the first goods acquired are the first costs charged to expense. Commonly known as FIFO.

Fraud – Wilful misrepresentation by one person of a fact inflicting damage on another person.

Generally Accepted Accounting Principles (GAAP) – Conventions, rules, and procedures necessary to define accepted accounting practice at a particular time. The highest level of such principles are set by the FINANCIAL ACCOUNTING STANDARDS BOARD (FASB).

Generally Accepted Auditing Standards (GAAS) – Standards set by the American Institute Of Certified Public Accountants (AICPA) which concern the AUDITOR’S professional qualities and judgement in the performance of his or her AUDIT and in the actual report.

Income Statement – Summary of the effect of REVENUES and expenses over a period of time.

Interest – Payment for the use or forbearance of money.

Internal Auditors – An independent group of experts in controls, accounting, and operations, who monitor operating results and financial records, evaluate internal controls, assist with increasing the efficiency and effectiveness of operations, and detect fraud within the company where employed.

Internal Revenue Code – Collection of tax rules of the federal government. Also referred to as Title 26 of the United States Code.

Inventory- Tangible property held for sale, or materials used in a production process to make a product.

Invoice – (or bill) a commercial document issued by a seller to the buyer, indicating the products, quantities, and agreed prices for products or services the seller has provided the buyer. An invoice indicates the buyer must pay the seller, according to the payment terms.

Journal – an accounting record in which transactions are first entered; provides a chronological record of all business activities.

Last in, First out (LIFO) – ACCOUNTING method of valuing inventory under which the costs of the last goods acquired are the first costs charged to expense. Commonly known as LIFO.

Ledger – Any book of ACCOUNTS containing the summaries of debit and credit entries.

Liability – DEBTS or obligations owed by one entity (DEBTOR) to another entity (CREDITOR) payable in money, goods, or services.

Liquidity – A company’s ability to meet current obligations with cash or other assets that can be quickly converted to cash.

No-Par Value – Stock or bond that does not have a specific value indicated. (See STATED VALUE.)

Par Value – Amount per share set in the ARTICLES OF INCORPORATION of a CORPORATION to be entered in the CAPITAL STOCKS account where it is left permanently and signifies a cushion of EQUITY capital for the protection of CREDITORS.

PCAOB – Public Corporation Accounting Oversight Board, a private-sector, non-profit corporation, created by the Sarbanes-Oxley Act of 2002 to oversee the AUDITORS of public companies in order to protect the interests of investors and further the public interest in the preparation of informative, fair, and independent audit reports.

Qualified Opinion – AUDIT opinion that states, except for the effect of a matter to which a qualification relates, the FINANCIAL STATEMENTS are fairly presented in accordance with GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP). The AUDITOR is required to qualify when there is a scope limitation.

Revenues – Increases in a company’s resources from the sale of goods or services; and earnings from INTEREST, DIVIDEND, rents.

Revenue Recognition Principle – The concept that revenues should be recorded when (1) the earnings process has been substantially completed and (2) an exchange has taken place.

Stated Value – Per share amount set by the BOARD OF DIRECTORS to be placed in the CAPITAL STOCK account upon issuance of NO-PAR VALUE.

Statement of Cash Flows: The financial statement that shows an entity’s cash inflows (receipts) and outflows (payments) during a period of time.

Statement of Financial Condition – Basic FINANCIAL STATEMENT, usually accompanied by appropriate DISCLOSURES that describe the basis of ACCOUNTING used in its preparation and presentation as of a specified date, the entity’s ASSETS, LIABILITIES and the EQUITY of its owners. Also known as BALANCE SHEET.

Transactions – Exchange of goods or services between entities (whether individuals, businesses, or other organizations), as well as other events having an economic impact on a business.

Unqualified Opinion – AUDIT opinion not qualified for any material scope restrictions nor departures from GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP). The AUDITOR may issue an unqualified opinion only when there are no identified material weaknesses and when there have been no restrictions on the scope of the auditor’s work. Also known as “clean opinion”.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

Meigs, Walter B. and Robert F. Meigs. Financial Accounting, 4th ed. McGraw-Hill, 1970, p.1

Accounting Terminology Guide, New York State Society of CPAs and Utah Association of Certified Public Accountants Accounting Glossary

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

Beyond the Fraud Triangle: Navigating Fraud Risks in Today’s Business Landscape

FRAUD. A five-letter word with consequential effects on individuals, organizations, and the economy as a whole. Fraud can be defined as an intentional act of deception in order to acquire something of value, whether it be a personal or financial...

How to Tackle Employee Fraud

Picture this, you, CFO, are sitting at your desk when an anonymous letter arrives alleging that employee X has been committing fraud against your company. Your first thoughts might be disbelief, anger and betrayal. You may question your relationship with...

Fraud Fighting 101

While I consider myself a pacifist, as a forensic accountant, I have been occasionally referred to as a fraud “fighter”. So, in the spirit of International Fraud Awareness Week (November 13 to 19, 2022), I would like to share some...

")

The ABCs of Cryptocurrency and Non-Fungible Tokens (“NFTs”)

Bitcoin. Ethereum. Litecoin. Dogecoin. NFTs. While they may seem like buzzwords or fads, cryptocurrencies or digital assets are experiencing a similar adoption pattern to the internet in the 1990s. In 1995, 14% of U.S. adults had internet access; by 2000,...

ESG Disputes and Business Valuation

Environmental, Social and Governance (“ESG”) factors have gained increasing importance in recent years as society has become more aware of how corporate conduct affects stakeholders, the environment and humanity at large. From issues such as climate change to socially responsible...

Business Valuation, Growth Rates and Climate Change: a Case Study of Vail Resorts

This past summer’s heatwaves and wildfires served for many as alarming reminders of climate change. Hotter summers, colder winters, and more hurricanes are amongst the symptoms of a changing global climate[1]. These climatic effects will impact different businesses in different...

COVID-19 and Fraud Claims

COVID-19 has sent shockwaves throughout much of the insurance world. Insurance company stocks have been some of the worst performing since the virus went, well… viral, in anticipation of declines in profits due in part to COVID-related claims. Much of...

COVID-19’s Impact On Business Valuation

This is the second blog post co-authored by MDW Law Partner, Christine Doucet, and MDD Forensic Accountants Partner, Jarrett Reaume, addressing various aspects of COVID-19’s impact on business owners and family law issues. Their first blog post was “Guideline Income...

Is Kylie Jenner a Billionaire, or Even Close? Part III

I hope this will be the final installment in this series, but one never knows. Back in the summer of 2018, I wrote a short piece questioning a sensational Forbes magazine article claiming that Kylie Jenner was worth $1B, based mainly...

Fraud in the time of COVID-19: Proactive steps to mitigate fraud risk

As the markets react to each update on COVID-19, a quote from Warren Buffet has seen increased circulation: “Only when the tide goes out do you see who’s been swimming naked”. The current environment has seen increasing news of corporate...

Is Kylie Jenner a Billionaire, or Even Close? Part II

A little over a year ago, I wrote a short blog post taking issue with a Forbes magazine article that had concluded that Kylie Jenner's net worth was around $900 million. In light of last week’s news that Coty Inc., a publicly traded cosmetics firm, is...

How Forensic Accountants Can Help You Manage and Effectively Resolve Litigation Cases

If you have not worked with forensic accountants before, an understanding of what they do in litigation support and how they differ from other accountants may be surprising to you. Modern television dramas’ common use of the word “forensic” may...

Adding up Cost of Construction Delays

No one likes delays. Whether it’s a rain delay at a sporting event or a subway delay stuck somewhere beneath the city of Toronto, delays cost us time that we would rather have spent doing something else. Sometimes, however, delays...

“Frenemies”: Is your organisation in bed with Brutus?

A growing area of concern for corporates is the proportion of fraud committed by “frenemies”, an encompassing term for the third parties a company works with on a day-to-day basis. This includes suppliers, agents and consumers: entities with which a...

The Better Way – Tips For Implementing Controls To Prevent Fraud

Last week, the Auditor General of Toronto issued a report estimating that in 2018 alone, the TTC lost $61 million due to fare evasion. As both a frequent rider of the TTC and a forensic accountant specializing in fraud investigations, I...

Financial Losses Resulting from LRT Construction

Introduction Some days it seems like you can’t go anywhere in Ontario without running into a light rail transit (“LRT”) project. Projects are either underway or imminent in Toronto, Hamilton, Ottawa and right here in Mississauga along Hurontario Drive. While...

Fraud and Corruption: How Culture Impacts Effective Risk Management

The Fraud Triangle: Rationalisation, Opportunity and Pressure Any elementary student of fraud will be aware of the “Fraud Triangle”, a theory developed by Edwin Sutherland and Donald Cressey. This theory posits three elements of fraud: Rationalisation (the ability of the...

Buying Shares in an NFL Player? Business Valuation Principles Still Apply

In my last post, I argued that an investor in Kylie Jenner’s cosmetics company was essentially investing in Ms. Jenner’s personal brand, and that the earnings stream for that brand was of a finite life. The post got me thinking:...

The Unique Perspective of a Certified ‘Forensic CPA’ Arbitrator

Alternate dispute resolution (ADR) is any procedure that is used in matters that would otherwise be settled in a court of law. Examples of ADR include arbitration, mediation, appraisal, and mini-trial. ADR is a dispute resolution strategy with applications to...

Is Kylie Jenner Really a Billionaire, Or Even Close?

A few weeks ago, Forbes created a social media storm when it proclaimed that Kylie Jenner was poised to become the world’s youngest self-made billionaire. Many thumbs were worn out debating the appropriateness of the term “self-made”, and apparently a GoFundMe page...

Valuing a Franchise System

Valuing a franchise system, or “franchisor”, is in many ways very similar to the valuation of any other type of business; it is a function of the forecasted levels of cash flows that the business will generate, and the risk...

Fidelity / Fraud Losses: Forensic Investigation and Loss Quantification Concepts

A fraudster’s gain is someone else’s pain – or loss; but is the corporate fraudster’s gain always the same as the insured’s financial loss? Are the financial implications of the fraud always the same as the actual loss to an...

How Much Is Your Business Worth?

As a Chartered Business Valuator (CBV), almost every business owner I meet wants to know the answer to this question: “How much is my business worth?” There can be many reasons for asking this question: they may be planning to...

What Type of Business Valuation Do I Need?

In my previous article, I discussed the critical need for business owners to have their business valued by a professional appraiser. In this article I will discuss the two types of business appraisals that you might want to consider. Calculation...

Should I Have My Business Valued?

What's so important about having a valuation of my company? Small business owners spend most of their time IN THEIR business and not ON THEIR business. Further, they view expending money on getting a professional valuation performed as a completely...

How to Protect Your Business Assets – What You Should Know

The most common response I hear from business owners who are victims of employee fraud is “I never thought this would happen to me”. Employee theft, especially in the automotive industry, is common, because small businesses such as car dealerships...

Business Valuations & Why It Pays To Use Genuine Experts

The Basics Assets have value if they will give rise to future economic benefits. For businesses, these future economic benefits take the form of either the expected net income stream or the amount that could be realised in the short...

Gift Cards and the Illiquidity Discount – A Valuation Perspective

With the busiest season of the year for retail sales upon us, you are no doubt wondering what to buy for that special someone. If you’re reading this blog – and I have every reason to believe you are –...

3 Tips On How To Protect Your Firm From Fraud & Internet Theft

While we’re thinking about turkey and cranberry, an important business holiday will come and go – not with the same fanfare as Thanksgiving perhaps but with significant potential for preserving the business future for those who take note. During International...

I Lost My Customers and It’s Your Fault!

In Schwartz Levitsky Feldman LLP v. Werbin, 2015, an action was put forward by Schwartz Levitsky Feldman (SLF) claiming loss of profits due to the departure of Mr. Werbin. The firm contended that they purchased Werbin’s clients when they purchased...

The Dividend Double Count

In this post, I touch on a common error I encounter in dealing with a financial analysis of multiple companies owned by the same group or individual. I call this error the “dividend double count”, for reasons that will become...

Adding up the Damage: Lost Profits vs. Business Value

When a business is destroyed as a result of wrongdoing, there are two commonly used methods by which the plaintiff’s damages may be measured. One method is to appraise the value of the plaintiff’s business at the date of loss;...

Calculated Risk: A $75M Award Adds Urgency to Pre-Judgment Interest Considerations

Pre-judgment interest is often the last thing litigants ponder. A recent award of $75 million in pre-judgment interest in Eli Lilly v. Apotex, 2014 FC 1254 (“Cefaclor”) may change that. Cefaclor involved the infringement of patents for an antibiotic. Damages...

Personal Injury Losses and the Self-employed: A Business Valuation Perspective on Labour & Capital

Business valuation concepts can be critical for the proper quantification of personal injury damages, particularly in the context of self-employed individuals. Business valuators are commonly called upon to assess the fair market value of small, owner-managed businesses. One of the...

5 Ways You Should Be Using Your Financial Expert

Moore v. Getahun 2015 ONCA 55 is a case that has already generated a lot of discussion and navel gazing in both the legal and expert communities, and I hesitated for quite a while before deciding that I had anything worthwhile to...

Dunkin’ Donuts c. Bertico inc., Part II: Lost Profit & Loss of Business Value

Towards the end of its decision in Dunkin’ Brands Canada Ltd. c. Bertico inc.2015 QCCA 624, the Quebec Court of Appeal discussed the issue of whether an award for both a) lost profits up to 2005 and b) loss of business...

Untying the Knot: A Forensic Accountant’s View of Divorce Proceedings

During the course of matrimonial disputes, there are often situations where solicitors find it helpful to engage specialist investigators and appraisers. In particular, forensic accountants can help to provide the court with a clearer view of the true financial position...

Mining Industry Revisits Anti-Corruption Procedures

Mining companies should take note of Canada’s stricter penalties and more aggressive enforcement of anti-corruption laws and make sure their anti-bribery compliance procedures are up to speed, lawyers, forensic accountants and mining executives warned at a recent conference in Toronto....

Rescission under the Ontario Arthur Wishart Act: Quantifying the Remedy

It has now been thirteen years since the Ontario Arthur Wishart (Franchise Disclosure) Act, 2000, SO 2000 [1], was enacted. The Act, named after Arthur Wishart, a Conservative MPP who championed the rights of franchisees in the 1970's and 1980's,...

Cheque Fraud – Who Is Responsible?

When a business falls victim to cheque fraud, it may look to its bank for recovery for allowing the fraudulent cheques to be cashed. In some recent cases, banks have been found liable and have been required to make whole...

Assessing Financial Motive

It is alleged that your client had financial motive to commit a very serious crime. Forensic accountants are often utilized to analyze the defendant’s financial records, and provide an opinion on the existence of financial circumstances that assist in assessing...

Accounting Fraud, Occupational Fraud & Abuse – A Clear & Present Danger to Your Business

The U.S. Chamber of Commerce estimates that occupational fraud costs U.S. businesses over $50 billion annually and that one-third of business failures are directly related to employee theft. The Chamber also estimates that 75% of all employees have stolen from...

Benford’s Law: A Powerful Tool for Uncovering Fraudulent Financial Transactions

Usually when you tell people that you’re a forensic accountant, you’re met with the same predictable and equally awful response: “So, you count dead peoples’ money?” Well, not exactly. It’s generally followed by something like, “You must be really good...

Accounting For Attorneys

It is becoming increasingly important for attorneys to understand financial statements and their relevance to various types of business and legal situations. The non-accountant attorney will greatly benefit from a basic understanding of the key principles of accounting. Equally important...

Financial Statements are Friends not Foes

Discovery is under-way. The records are starting to flow. As you leaf through a box of documents just delivered, you pull out a stack of financial statements and, like so many other attorneys, you cringe. As you scan through the...

How Can a Forensic Accountant Assist with Surety Claims?

New construction is a key component of the economic growth, with commercial construction among the leading sources of new jobs and increased capital spending in practically every geographical market. With millions of dollars on the line for investors, construction companies,...

Are Risks Hiding in the way your Revenues and “Expenses” are Reported?

Are you concerned about how your employees can get around your accounting policies or what unintended impact they might have? Here are two areas where accounting policies may pose a risk. Revenue Recognition Revenue recognition is always on the mind...

Quantifying Business Loss Involving Expropriation of Newly Established Businesses

With increasing activity in public works projects in the Greater Toronto Area (e.g. the Toronto-York Spadina Subway extension) and other highway expansions across Ontario, we can expect a large number of businesses to be affected by expropriation. This article will...

5 Steps to Investigating Fidelity Claims

Fidelity losses are difficult to investigate because frauds can be complex and hard to detect. Here are 5 steps to keep in mind when assessing fidelity claims. Understand business and accounting system Identify who performs the accounting duties and the documents generated...

Documentation and Litigation

Litigation can be a scary and intimidating process. Preparation is key and includes ensuring that the documentation you need to prove your case is ready at hand. Below are some common forms of litigation and the documentation that should be...

Forensic Accountants Make It Add Up

Corporate fraud, insider trading, 9/11, intellectual property infringement the list goes on as to instances where parties have committed acts resulting in financial losses. The legal challenge in proving financial wrongdoing is a minefield in itself, but what steps need...

Fight the Battle on Two Fronts – Liability and Damages

Plaintiff and Defense attorneys are guilty! Guilty of waiting until the last minute to address areas of damages. MDD is very often retained in litigation engagements when the measurement of damages takes a back seat to liability and causation. Although...

The Role of a Forensic Accountant as an Expert Consultant and an Expert Witness

For many years, attorneys on both sides of the courtroom have turned to forensic experts to support their position as well as to identify the potential strengths and weaknesses in the arguments of opposing counsel. Additionally, attorneys can use expert...

Business Valuations: When You Would Need One

Business valuations in one form or another have been around for decades. As a result of the Eighteenth Amendment to the United States Constitution, the Internal Revenue Service began issuing memorandums and directives relating to methods for determining values and...