CAT Insights – The Increasing Risk and Frequency of Wildfires

23 October, 2023

23 October, 2023-

Lisa Morris

Lisa Morris -

USA

USA

Depending on where you are located, you are likely to experience some sort of “weather disaster season,” such as hurricane season, cyclone season, tornado season, earthquake season, or wildfire season. I live in California where we have earthquake season, which is year-round, and in the last 7 years, I have become increasingly familiar with wildfire season.

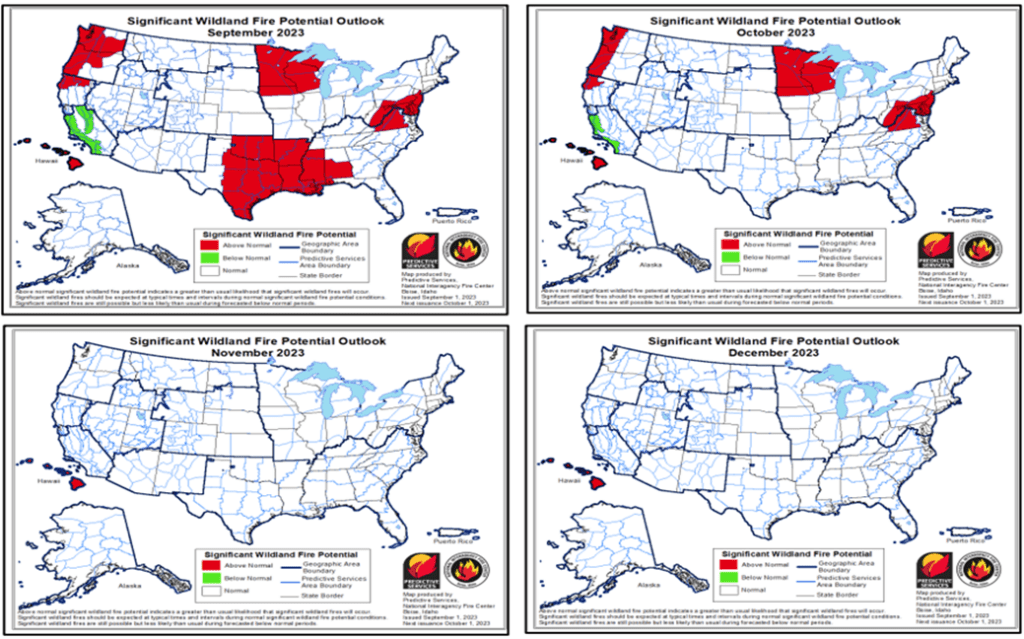

The National Interagency Fire Center (NIFC) issued a report on September 2, 2023, which shows above-normal wildfire potential for the rest of the wildfire season for various parts of the country due to hot and dry conditions in some areas and long-term drought in others. In California, it finally rained and the NIFC stated we should have lower-than-normal wildfire potential for the rest of the season.[1].

Although I have been in forensic accounting for 25 years and have seen the impact of hurricane season a multitude of times, only in the last 7 years have I really seen the impact of wildfire season.

With a hurricane, people often have warning. The weather service sees the hurricane coming and informs people to the best of their ability, of the likely impact of the storm. The hurricane does not normally hang around for days at a time. When deemed safe, people have access to their property to determine the extent of the damage, what could be saved, and what needed to be leveled or repaired.

When a wildfire hits, often there is no time for preparation. The weather service has not been covering the fire for days trying to predict its trajectory. The fire starts and can move at incredible speeds. I remember listening to a news report related to the Camp Fire in Paradise, which stated the fire spread the length of an American football field in a matter of approximately 60 seconds.

With a wildfire, it can be days or weeks until the fire is contained. People are evacuated and left wondering what they will find when they are allowed to return. The wildfire can change direction quickly, as embers are carried by the wind, such that one structure will be burned, and the neighboring building is left unscathed. With a fire, some structures have smoke damage, some have water damage from firefighting activity, and some are burned to the ground with not much evidence left of what was inside.

Depending on the extent of the damage from the fire, we have seen issues such as:

- The inability for insureds to reopen due to contaminated water supplies, as was seen with Benzene in the Camp Fire in Paradise

- Increased periods of repair due to a shortage of materials and trades to perform the work, as was seen in the Atlas fire in Napa in 2017 and the Glass fire in Napa/Sonoma in 2020

- Insureds not rebuilding at the loss location due to the loss of an entire city/town as their customers have also moved away due to the destruction of their homes

- Insureds with losses at different locations under their umbrella in both the 2017 and 2020 wildfires

- COVID impact on insured’s businesses which sustained damage in the wildfires

Wildfires in the California wine country bring their own unique circumstances. Having performed calculations for a multitude of wineries over the years, when the assignments started coming in, we had immediate questions such as:

- Where in the crush process was the winery?

- Were the grapes harvested? If so, where were they stored?

- Had the grapes been crushed and not yet yeasted?

- Did the fire destroy the vines?

- Was there damage to the wine?

- If so, in what stage of fermentation was the wine when the fire hit?

- Was there damage to the storage vessel?

- When was it to be bottled and/or sold?

The answers to these questions have an impact on coverage and valuation. We worked with wineries that were in the middle of crush season and the smoke had permeated the skins of the grapes and/or had permeated the vessel in which the wine had been stored. This had caused “smoke taint” to the grapes/wine. In some instances, the insured was able to mitigate the loss of revenue by still selling the wines, but the wines had been “degraded.” The insured was not able to sell the wine as intended but was able to sell it as a blend, at a lower price point, or on the bulk market. Other wineries had been able to produce the wine without using grape skins, so the wine was free of smoke taint.

Thankfully at MDD, we have experience working on claims where there are unusual circumstances. We can draw on our personal experience handling claims or reach out to our network of professionals around the globe to draw on the knowledge of others.

If you would like to draw on our knowledge, please click here.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

[1] National Significant Wildland Fire Potential Outlook (nifc.gov)

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

Measuring Business Interruption Claims: A Case Study From Christchurch and Kaikoura Earthquakes

Earthquakes are a historically prominent event in New Zealand, occurring most commonly in the Southern and Eastern areas of the North Island and most of the South Island. This is because New Zealand falls over the Australian and Pacific tectonic...

MDD LA Wildfires Report

California Wildfires of January 2025: A Devastating Start to the Year The year 2025 began with a series of devastating wildfires that swept through Southern California, leaving a trail of destruction and significant insured losses in their wake. Fuelled by...

CAT Spotlight – Iceland

In this CAT spotlight, we focus on Iceland, situated on the Mid-Atlantic Ridge, a country prone to volcanic eruptions, earthquakes, and glacial floods. The most well-known CAT event in recent times was the March 2010 Eyjafjallajökull eruption. Most will remember...

Recapping the 2024 Hurricane Season

Whilst to most, 01 December marks the countdown towards the festive season, to others on the other side of the Atlantic, it also marks the end of the Hurricane Season (officially on 30 November). Initial Forecast vs. Actual Season Forecast Expectations:...

CAT Spotlight – Italy

In this CAT spotlight article, we look at Italy, where floods and earthquakes have caused the most damage over the last two centuries. As an example of the frequency of seismic events, Italy suffered over 16,000 in 2023, according to...

Measuring Business Interruption Dependency Claims: A Case Study from Cyclone Gabrielle

Cyclone Gabrielle made history as the costliest tropical cyclone in the southern hemisphere. Conceived as a tropical low North of Fiji in early February 2023, Cyclone Gabrielle intensified to as high as Category 3 storm. After downgrading to ex-tropical cyclone...

The Bottom Line of Catastrophe: How Catastrophic (CAT) Events are Impacting the Insurance Industry Worldwide

In this new series of spotlight articles, we look at how CATs are affecting different countries all over the world. These are snapshots of various countries CAT history and are designed to give the reader a basic understanding of the...

Floods in the South of Germany in June 2024: Highly Complex Business Interruption Losses

At the beginning of June 2024, unusually high precipitation occurred in large parts of southern Germany. This resulted in flooding and in property damage to residential and commercial properties over a large area. Initial estimates provided by the German insurance...

Predictions for the 2024 Hurricane Season: Implications for the Insurance Industry

“May 2024 (Tortola): it’s currently 30 degrees (Celsius) down there…” I’ve been very fortunate to experience first-hand the beauty of the Caribbean over the past few years, but you could imagine my surprise, when the diving instructor mentioned the above...

How Can a Forensic Accountant Assist With a Dairy Farm Loss?

How can a forensic accountant assist with a dairy farm loss? Typically, a trigger event causes a farm to impede its operations. MDD may be retained when this occurs to quantify the loss from milking operations or other aspects. Background...

El Niño – Weather Phenomenon & Global Disruptor

What is “El Niño”? In normal conditions in the Pacific Ocean, the trade winds blow westerly along the equator, bringing warm water from around South America towards Asia. In a process known as “upwelling”, cold water from the depths of...

CAT Insights – The Increasing Risk and Frequency of Wildfires

Depending on where you are located, you are likely to experience some sort of “weather disaster season,” such as hurricane season, cyclone season, tornado season, earthquake season, or wildfire season. I live in California where we have earthquake season, which...

Natural Catastrophe Insurance Coverage in Asia: An Overview

Natural Catastrophes in Asia In 2021, Asia was the most severely impacted region, experiencing 40.00% of all disaster events, 49.00% of total deaths, 66.00% of the total number of people affected and 18.90% of all natural catastrophe economic losses worldwide...

Property Damage and Derechos

On 29th June 2023, a rare type of storm called a "derecho" swept across the Midwest region of the United States, mostly impacting the states of Missouri, Illinois and Iowa. The derecho began as a rotating supercell thunderstorm that spawned...

The Broader Impact of CAT Events

While every catastrophe (“CAT event”) leaves a wake of destruction in its path, there are times when the financial impact is more widespread than the physical damage would indicate. Consider the following examples: Pandemic – 2020 The impact of COVID-19...

What to Do When Disaster Strikes & You Can’t Access Financial Documents

Swiss Re’s website sigma-explorer.com noted insured losses for 170 natural catastrophes and 105 man-made disasters in 2021 alone.[i] While almost all of these events resulted in property damage and loss of earnings for the affected businesses, some of those entities...

Calculating the Effects of a Natural Disaster

The Allianz Risk Barometer 2022 reported that natural catastrophes are now the third-highest global business risk, while climate change has moved into the sixth position. These rankings represent 25% and 17% increases from last year.[i] Furthermore, the increasing complexity of...

Lost Profits Measurement in the Cannabis Industry

What used to be considered an illicit drug in most countries is now a decriminalized plant with some medicinal potential. Cannabis is in the midst of a global transformation into a major industry with massive investment and growth potential. Canada...

Trends in Food and Beverage Related Product Recalls

Numerous large-scale product recalls have captured national, if not global, media attention. One example is the 2008 salmonella outbreak linked to products manufactured by the Peanut Corporation of America. This incident involved the recall of more than 4,000 products produced...

The Varying Effects of a La Niña Cycle on Business Interruption Claims

Earlier this month, Australia’s Bureau of Meteorology announced that the current La Niña conditions would likely continue over the coming months.[i] According to the National Oceanic and Atmospheric Administration, the La Niña effect occurs when there are “periods of below-average...

Business Interruption Measurement Considerations in a COVID-19 World

Although hurricane season doesn’t normally conclude until November 30th, we have already exhausted the modern English alphabet in terms of named hurricanes. In the last year, we’ve also seen an ever increasing number of wildfires, explosions and tropical storms. While...

The Triple Threat: Pandemic, Natural Catastrophe and Business Interruption

Calculating business interruption losses following a natural catastrophe (“CAT”) has always been as much of an art as a science, requiring forensic accountants to use their education, experience and training to resolve the complexities inherently present in quantifying business interruption...

Claim Considerations Related to the Beirut Port Explosion – Part 2

On 17 October 2019 large numbers of protesters began appearing in Martyrs Square, Nejmeh Square, and Hamra Street, as well as many other areas of Beirut and throughout Lebanon. The reasons for the protests are wide reaching from a social,...

Claim Considerations Related to the Beirut Port Explosion – Part 1

In this two-part series, we write about the claim considerations related to the Beirut port explosion on 4 August 2020. On 4 August 2020 at approximately 18:00 local time, an explosion measuring 3.3 on the Richter scale ripped through Beirut...

Is the Perfect Storm Brewing?

Insurers around the globe currently have their attention firmly fixed on addressing the enormity of client claims relating to COVID-19 but is there another dark cloud gathering on the horizon? Recent scientific information includes NOAA issuing their forecast on May...

Business Interruption Losses Involving Dairy Farms

As anyone who followed the debate over the USMCA trade agreement last fall will know, Canada’s dairy industry is a regulated one. As a result, business interruption calculations involving dairy farms will often contain a number of moving parts that...

Caribbean ‘vacation’ for CAT claims

As a global forensic accounting firm, we at MDD have a “boots on the ground” mentality when it comes to quantifying economic damages for catastrophe (“CAT”) claims. The busy hurricane season in 2017 meant that I, along with many of...

Mexican Standoff – Insured Losses in Mexico Following Recent Catastrophes

September 2017 was a brutal month for the people of Mexico, with two earthquakes and a hurricane causing untold misery, multiple deaths and substantial property damage across the country. But if the general view in the global reinsurance market is...

Business Interruption Insurance and Dealing with Natural Catastrophe Events

Late 2017 has witnessed a flurry of catastrophic weather events that has led to widespread devastation. Hurricane Harvey set the ball rolling, with unprecedented rainfall in the southern United States. Irma then destroyed several Caribbean islands, rendering many uninhabitable, before...

Cyclone Debbie May Create Complex Claims Issues for Insurers

Cyclone Debbie and the subsequent rain and flooding events across Queensland, Northern NSW and New Zealand have caused significant damage to property and infrastructure, limited rail access, closed ports and caused damage to numerous roads and bridges. Rail closures in...

Financial Impact of New Zealand Kaikoura Earthquakes Felt Beyond Earthquake Zone

While the damage to physical property as a result of the Kaikoura earthquakes in November 2016 has been well documented, the financial impact of these events are ongoing both on businesses physically affected by the earthquakes as well as businesses...

Staying Afloat in the Flood – The Cost of Flooding to Companies with Exposures in India

Given the number of major flood occurrences in India in the past decade, European and US companies with exposures in the country should examine their insurance coverage and disaster management planning. As the waters start to subside following India’s latest...

Canadian Wildfire Present Challenges to Business Owners and Their Insurers

The Canadian wildfire which started in early May 2016 southwest of Fort McMurray affected a population of about 90,000 and led to destruction of over 2,400 structures. The sheer ferocity and speed of the fire took both public services and...

Catastrophe Events and Business Interruption Insurance

In the event of a devastating catastrophe (“cat”) be it an earthquake, hurricane, flood, or tornado, the first and foremost priority is to ensure the safety all the people involved. Once this has been established, business owners can then begin...

Dunkin’ Donuts c. Bertico inc., Part II: Lost Profit & Loss of Business Value

Towards the end of its decision in Dunkin’ Brands Canada Ltd. c. Bertico inc.2015 QCCA 624, the Quebec Court of Appeal discussed the issue of whether an award for both a) lost profits up to 2005 and b) loss of business...

Dunkin’ Donuts c. Berticoinc, Part I: The Benchmark Approach to Lost Profits

In April 2015, the Quebec Court of Appeal released its decision in Dunkin’ Brands Canada Ltd. c. Bertico inc. 2015 QCCA 624. The Court of Appeal upheld the trial judge’s ruling (Bertico inc. c. Dunkin' Brands Canada Ltd., 2012 QCCS 2809) that...

Agricultural Loss – Quantifying Economic Damage for a Hog Farm

Damage quantification for livestock losses can be difficult as it often requires consideration of market price fluctuations, age and weight of livestock at the time of loss and the end purpose of the livestock - considering whether they are for...

Proving Rescission Damages under the Provincial Franchise Acts

In October 2012, the Manitoba Franchise Act was proclaimed into law. The legislation, like its counterparts in several other provinces (including Ontario’s Arthur Wishart Act), provides franchisees with the right to rescind a franchise agreement within two years if a...

What to do When You Can’t Get to Documents

On June 20, 2013 Southern Alberta endured a catastrophic flood resulting in a significant amount of property damage, numerous civil authority evacuations and power outages for individuals and businesses. In any major catastrophe, access to supporting documentation may not be...

The Forensic Accountant’s Role in a Large Loss

No matter how well a risk management team has planned for it, actually dealing with a catastrophe can be a distracting and stressful financial challenge. The adjuster's ability to manage his resources and work through the complex claim issues that...