The Recovery of Oil & Gas: A Roller Coaster Ride or Merely a Few Speed Bumps?

04 October, 2021

04 October, 2021-

Phillip Taylor

Phillip Taylor

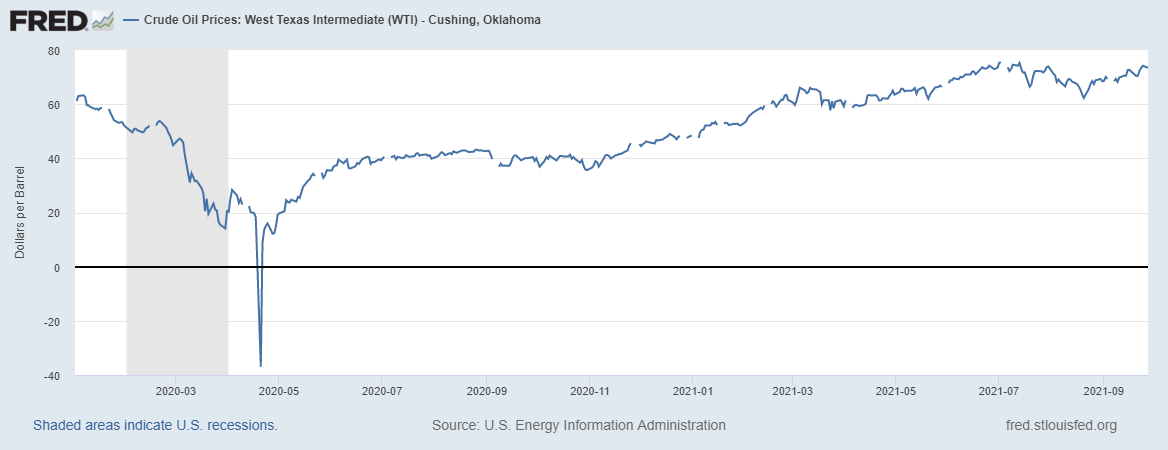

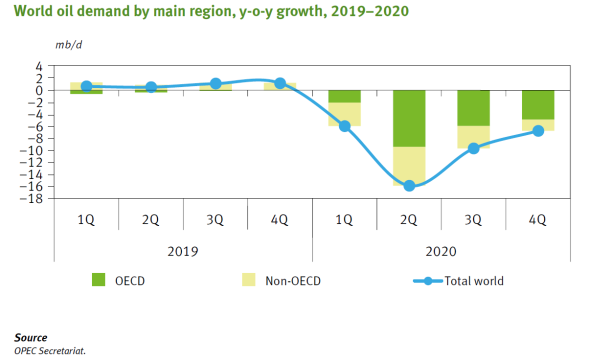

Covid-19 has led to major disruptions across various sectors and the petroleum industry is no exception. Demand for oil and petroleum products, in general, declined due to reduced economic activity as governments worldwide imposed lockdowns and tightened border controls. Certain sectors, such as aviation and transportation, were particularly affected and prices of gasoline, diesel and jet fuel tumbled as a result. Naturally, this had an impact on upstream processes as well. Refineries began to alter their output mix, run at reduced rates or even shut down entirely in the face of adverse market conditions, while US crude prices briefly veered into negative territory over concerns about excess supply and insufficient storage capacity (see Chart 1 below). Overall, world oil demand declined by 9.6 million barrels per day from 2019 to 2020 according to OPEC estimates (see Chart 2 below).

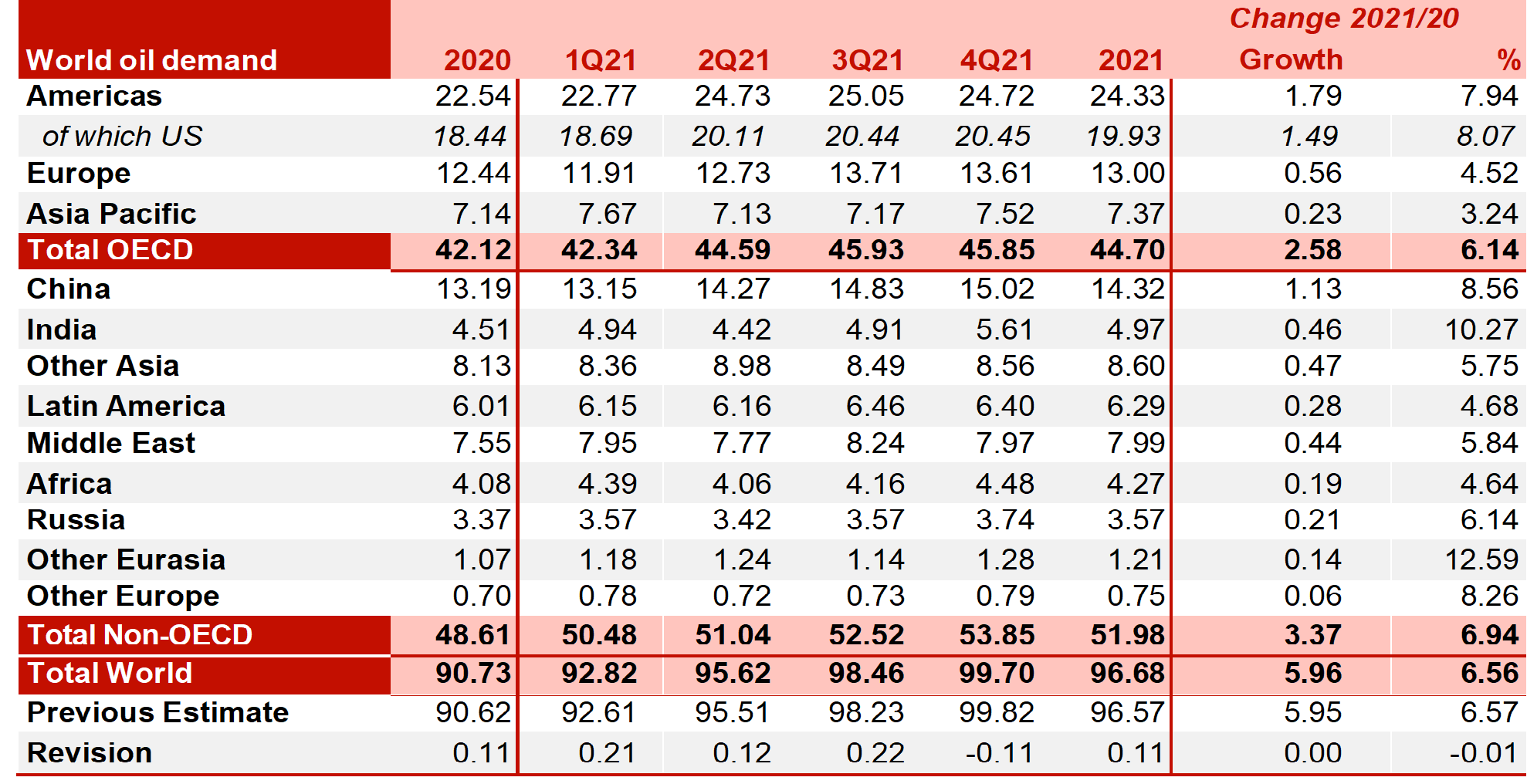

As the world adapted to living with the pandemic, supported in part by substantial stimulus packages, economic activity has begun to recover. This optimism has been further bolstered by successful vaccine rollouts and subsequent lifting of pandemic restrictions across a number of countries. Although there has been increasing attention on green energy and sustainability in recent years, fuels derived from crude oil remain crucial to meeting energy needs and various industries continue to utilise petrochemicals within their processes. As such, demand for oil and petroleum products has picked up (see Table 1 below) and, in a number of instances, prices have exceeded pre-pandemic levels. Nonetheless, as the past two years have shown, it is impossible to predict the future with a high degree of certainty and the trajectory of the recovery remains to be seen.

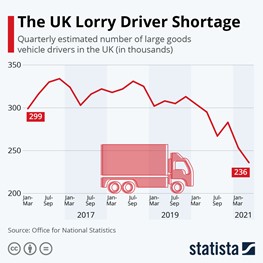

In spite of this recovery, motorists across the UK have struggled to fill up their vehicles in the past week as forecourts dried up and were unable to be replenished in time. Industry and government spokesmen have emphasised that there is no shortage of petrol and diesel as ample supplies are available at refineries. The root cause of this crisis has been identified as a shortage of heavy-goods vehicle (HGV) drivers (see Chart 3 below), brought about by a perfect storm of various factors, including Brexit, the pandemic as well as inadequate pay and working conditions. In recent days, alleviating measures such as deploying Army resources, relaxation of competition laws and a short-term visa scheme for foreign HGV drivers have been announced, although experts warn this is a long-term structural issue. This recent turn of events serves as a reminder that where complex supply chains exist, general industry trends may not necessarily apply and the recovery from a period of depressed activity might take longer than expected.

From an insurance perspective, price volatility can certainly lead to volatility in refining and petrochemical margins. However, higher oil and gas prices do not automatically mean higher business interruption claims – this topic will be explored in-depth in one of our future Oil & Gas technical briefings in the coming months.

By Yiyan Lin and Phillip Taylor.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

Chart 1: WTI Crude Oil Prices

Chart 2: Global Oil Consumption Growth – Year 2019 to Year 2020

Table 1: World Oil Demand in 2020 and 2021

Chart 3: Number of HGV Drivers in UK, by Quarter

Phillip Taylor

FCMA, CGMA, CFE, Chief Operating Officer – EMEA & APAC

- ptaylor@mdd.com

- Singapore, APAC

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

How is Electrification Disrupting the Energy Sector?

One of the biggest trends shaping society today is the widespread adoption of Electric Vehicles (EVs). While Tesla pioneered this movement as a disruptor, nearly every automobile manufacturer worldwide is now actively developing its own electric vehicles. Governments have implemented...

Carbon Capture – Is it Really Going to Materialise?

Before we discuss the carbon capture process and how it is used, it is worthwhile conceptualising the carbon emissions emitted worldwide and why different technologies, including carbon capture, must be considered as part of the energy transition. As can be...

Natural Gas – The Past, Present and Future

There has been a significant push towards transitioning to cleaner and renewable energy sources, moving away from fossil fuels due to their environmental impact. By looking at the past, the present and the future, the question remains: can we realistically...

Upstream Oil and Gas Losses

In this briefing, we discuss various considerations in upstream oil and gas production losses, and in particular how rates of production depend on the type of well. We also discuss what the shift to horizontal drilling and hydraulic fracturing means...

An Introduction to Natural Gas: Separation, LNG and GTL Plants

Our first technical briefing introduced the Oil & Gas value chain, divided into: i) upstream; ii) midstream; and iii) downstream. Here is a recap, before we explore natural gas in more detail. Upstream: this involves the exploration and extraction of...

Imbalance of Gas Supply

The sanctions imposed on Russia amid the Russia-Ukraine conflict have impacted global gas markets, particularly those in Europe. Russia is the second largest producer of natural gas globally and used to supply about 40% of Europe's natural gas. However, supplies...

The Global Energy Crisis

As the Ukrainian conflict unfolds, Europe’s energy dependence on Russia becomes an increasingly critical bargaining tool. The economic sanctions imposed by some Western nations in response to Russia’s invasion appear to be increasingly directed against Russian oil and gas supplies...

Measuring Refining Margins for a BI Loss

When it comes to Business Interruption policies for Oil & Gas risks, there are different types of coverage available in the market, including Gross Profit, Gross Earnings, Specified Standing Charges etc. Common Policy Wordings Gross Profit equates to Turnover less...

in Refinery Claims")

The Importance of Linear Programs (LPs) in Refinery Claims

The use of Linear Program models is common in refining, and other industries, to optimise their activities by using an algorithm subject to a set of inputs, constraints, and relationships. This article discusses the LP models in more detail and...

What Happened to Jet Fuel During Covid-19?

The main types of jet fuels used by airlines are Jet A-1, Jet A and Jet B. Jet A is mainly used in the United States, whereas Jet A-1 is commonly used outside the United States and Jet B is...

The Recovery of Oil & Gas: A Roller Coaster Ride or Merely a Few Speed Bumps?

Covid-19 has led to major disruptions across various sectors and the petroleum industry is no exception. Demand for oil and petroleum products, in general, declined due to reduced economic activity as governments worldwide imposed lockdowns and tightened border controls. Certain...

What Triggered the UK Energy Market Crisis and What is the Impact on BI Claims?

The UK’s energy wholesale markets have reached new highs, with daily average electricity prices rising above GBP 150 per MWh since early September 2021. A record high of GBP 424 per MWh, since at least January 2019, was reached on...

Introduction to the Oil & Gas Value Chain

The Oil and Gas industry in the insurance market is usually categorised between Onshore/Offshore or Upstream/Downstream. It includes a chain of businesses relating to extraction, transportation, refining, petrochemical and chemical – essentially from the carbon in the ground to the...

The Effect of Deductibles & Policy Wording – Is It What You Think?

With a typical Energy claim standing at approximately USD 4.5 million, it’s no surprise that Business Interruption (BI) is once again the #1 business risk for the fourth year in a row[i]. To help insurers mitigate their exposure when an...

Court Breaks with Apportionment

The case of Varco Canada Limited v. Pason Systems Corp., 2013 FC 750 (CanLII) involved an award of over $52M based on an accounting of the defendant’s profits. Perhaps more importantly, the decision sheds light on a number of conceptual...