The Unique Perspective of a Certified ‘Forensic CPA’ Arbitrator

23 August, 2018

23 August, 2018 John Damico

John Damico USA

USA

Alternate dispute resolution (ADR) is any procedure that is used in matters that would otherwise be settled in a court of law. Examples of ADR include arbitration, mediation, appraisal, and mini-trial. ADR is a dispute resolution strategy with applications to insurance, reinsurance, commercial contract and/ or labor disputes, estate and divorce actions, and personal injury claims.

ADR procedures generally offer a less emotional, more cooperative approach and allow each side to better understand the other’s position without legal wrangling. When used effectively, ADR is more efficient, takes less time, and is less costly. Experienced arbitrators and mediators can often guide a more creative process tailored to the specifics of the dispute in question.

Role of the Forensic CPA

Historically, forensic CPAs (FAs) participate as experts alongside attorneys, other subject-matter experts, and claim handlers representing either the claimant or respondent in insurance and reinsurance disputes. For the moment, consider how resolving these disputes through ADR might benefit from the experience of a seasoned FA as an arbitrator or mediator.

First, it is not uncommon for FAs, in their role as experts, to represent both claimants and respondents. Having participated on both sides of the table provides FAs with a valuable perspective when discharging their arbitrator or mediator responsibilities.

In addition, FAs bring many other advantages to the dispute resolution process:

- Because they are also certified public accountants (CPAs), FAs have extensive experience analyzing financial statements, operating systems, manufacturing processes, and business operations in general as they delve into the damages, claimed and disputed amounts (‘the quantum’), and supporting accounting details. They are comfortable working with the numbers.

- As CPAs, FAs practice under the Professional Code of Conduct of the American Institute of Certified Public Accountants (AICPA). The code’s standards of objectivity, independence and due care are ingrained into the DNA of FAs. The AICPA code parallels the ethical codes applicable to arbitrators and mediators in its emphasis on integrity, honesty, fairness and competence.

- While technically not viewed as “policy experts on insurance matters,” seasoned FAs nonetheless have considerable experience examining and applying the various types of coverage to claim disputes as they categorize and quantify the loss components into appropriate “coverage buckets.” They understand how coverage works in real-life terms.

- FAs are accustomed to analyzing the deep quantum details, reconciling the claim differences on a line-by-line basis, and presenting their findings to the parties. This can be especially helpful in highly complex claims, such as the case of overlapping covered and excluded physical damage and resulting business income and extra expense losses where a seemingly minor change in one of the variables has an unexpected ripple effect, magnifying the amount of loss.

- As a mediator, an FA is well equipped to help the parties identify and prioritize the dollars associated with issues most important to each side as they attempt to reach a settlement. Similarly, as an arbitrator, the FA is well-positioned to help other panel members evaluate and reach agreement on how a dispute should be resolved.

- FAs who have represented both claimants and respondents bring a level of impartiality and a unique perspective to the mediation or decision-making process.

- Forensic accounting may be generally defined as “the art and science of investigating people and money.” As such, the FA’s investigative skill set includes a keen sense of what’s fact versus fiction as well as what’s reasonable as opposed to speculative.

By Way of Example

What follows is a hypothetical first-party property insurance dispute that illustrates how an FA’s experience and skill set might be used effectively to address some of the challenges that an arbitrator or mediator might face in an ADR proceeding.

Assume that a policyholder incurs a total physical damage loss at its Alabama plant. The plant provides important parts to another of its up-stream assembly plants in Michigan. As the insured scrambles to find an alternate source of supply parts to mitigate its loss exposure, it quickly decides to seize the opportunity to expand and modernize the Alabama plant during the downtime. These decisions trigger policy coverage and quantum measurement issues for both the property damage and time element (business income and extra expense) losses.

Setting aside “like kind” replacement cost issues affecting the amount of property loss, the policyholder’s decision to expand and modify the Alabama plant creates a mix of other coverage and loss measurement issues. One obvious issue is the need to determine a theoretical versus actual peiod of indemnity (POI) to repair and replace the property as it was at the date of loss. A related issue is what and how much are the business income and extra expense components of the losses sustained during the applicable POI.

Faced with these issues, an FA arbitrator or mediator can easily reconcile the major components of the loss in dispute that lead to a more informed resolution. Rather than using some arbitrary approaches such as splitting the difference, the baseball high/low, or another similar “compromise” approach, reconciling the damages with the coverage issues is a pragmatic way to focus on the real dollar differences and provide a framework in which each side’s position can be prioritized or ranked from strongest to weakest. The FA mediator can facilitate the parties in their attempt to reach and agree upon a settlement; likewise, an FA arbitrator is well-positioned to reach an informed and principle-based decision.

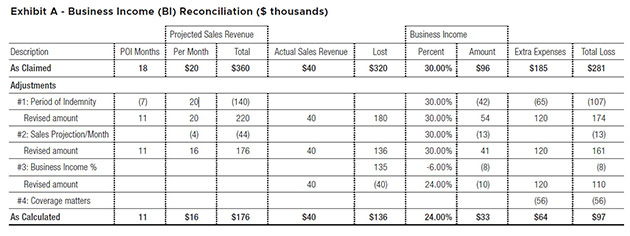

Refer to Exhibit A above to see what a reconciliation in the case of the above time element loss hypothetical might look like. The analysis begins by identifying all the major as-claimed categories across the top of a spreadsheet. The next steps are designed to allow only one adjustment at a time to account for each major difference until one reaches the as-calculated amount detailed at the bottom of the spreadsheet.

Now let’s walk through Exhibit A above and further discuss how a basic time element/business income reconciliation works. For purposes of this hypothetical, assume the policyholder has made a business income (BI) claim based on an 18-month period of indemnity (POI) and has claimed $96,000 in BI and another $185,000 in extra expenses (EE) for a total claimed amount of $281,000. Major differences between the parties are illustrated as adjustments 1 through 4 below:

- #1: Period of Indemnity. There is a difference of seven months between the time it took for the insured to expand and modernize the Alabama plant as opposed to the theoretical period of indemnity it should have taken to repair and replace the plant as it was at the time of loss with due diligence and dispatch. Therefore, the amount of BI/ EE loss solely attributable to this time factor is a $107,000 difference.

- #2 Projected monthly sales revenue. Based on some differences in trending methods and an error in calculation, the insurer’s position is that expected monthly sales revenues had no loss occurred would have been $16,000. This adjustment results in a $13,000 difference on a stand-alone basis.

- #3 Business income (BI) percentage. The parties could not agree on the appropriate BI gross-earnings-less-non-continuing-expenses percentage to be applied to the amount of lost sales revenue. This adjustment creates an $8,000 difference, again on a stand-alone basis.

- #4 Coverage matters. Due to some differences in coverage, the parties could not resolve this area. This adjustment results in a straightforward difference of $56,000.

The FA and the parties can now identify how many dollars are associated with each of the major differences in the dispute. The panel can then prioritize based on the perceived strengths and weaknesses of each party’s position as they move toward a more informed resolution of the dispute.

No Strangers to Coverage

Matching the right mediator or arbitrator to the specific facts and issues in dispute is crucial to a successful ADR outcome. Adding an FA to the potential pool of candidates introduces a different perspective and set of skills that should not be overlooked. FAs are no strangers to coverage; in fact, they often have a better appreciation of the real-life impact because of their ability to quantify the financial loss by varying the coverage equation. They are comfortable working with financial concepts and numbers and are accustomed to devising reconciliation tools that can be used to simplify complex disputes, thus leading to a fair ADR resolution.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

Role of a Forensic Accountant in Divorce

During the course of matrimonial disputes, there are often situations where solicitors and their clients find it helpful to engage specialist consultants. Forensic accountants can assist at various stages of divorce proceedings, in order to provide a clearer picture of...

COVID-19’s Impact On Business Valuation

This is the second blog post co-authored by MDW Law Partner, Christine Doucet, and MDD Forensic Accountants Partner, Jarrett Reaume, addressing various aspects of COVID-19’s impact on business owners and family law issues. Their first blog post was “Guideline Income...

Guideline Income for Business Owners in the Wake of COVID-19

Business owners don’t need an economist to tell them how dramatically their profits have been affected by the COVID-19 pandemic. For those owners who are separated from their spouse, these poor results are impacting how much “available income” they have...

How Forensic Accountants Can Help You Manage and Effectively Resolve Litigation Cases

If you have not worked with forensic accountants before, an understanding of what they do in litigation support and how they differ from other accountants may be surprising to you. Modern television dramas’ common use of the word “forensic” may...

The Unique Perspective of a Certified ‘Forensic CPA’ Arbitrator

Alternate dispute resolution (ADR) is any procedure that is used in matters that would otherwise be settled in a court of law. Examples of ADR include arbitration, mediation, appraisal, and mini-trial. ADR is a dispute resolution strategy with applications to...

Economic Damages from Personal Injury: A Forensic Accountant’s Perspective

Regrettably, individuals can experience a temporary or permanent diminishment in their ability to perform certain functions due to a tortfeasor. Forensic accountants and economists are regularly retained in matters involving the injury or death of an individual for the purpose...

Class Action Lawsuit – What Do You Do Now?

It’s happened. You find your company is facing the business end of a class action lawsuit. Perhaps this stemmed from your product not meeting customers’ expectations or maybe there are allegations that your product is not performing as advertised. Now...

Business Valuations & Why It Pays To Use Genuine Experts

The Basics Assets have value if they will give rise to future economic benefits. For businesses, these future economic benefits take the form of either the expected net income stream or the amount that could be realised in the short...

Calculating Sports Star Damages

The lawsuit of Canadian tennis star Eugenie Bouchard v. United States Tennis Association is still at an early stage. However, as forensic accountants who spend much of their time thinking about personal injury damages and playing tennis (albeit poorly), it...

Real Injuries, False Returns: Personal Injury Claims and Unreported Income

Individuals advancing claims for loss of income due to bodily injury may have historically underreported their income to the taxation authorities. A 2011 Statistics Canada study estimated the size of Canada’s “underground economy” at up to $36 billion. Other research...

Personal Injury Losses and the Self-employed: A Business Valuation Perspective on Labour & Capital

Business valuation concepts can be critical for the proper quantification of personal injury damages, particularly in the context of self-employed individuals. Business valuators are commonly called upon to assess the fair market value of small, owner-managed businesses. One of the...

Personal Injury Damages and the “Capital Asset” Approach

Canadian courts have typically adopted one of two categories in quantifying financial losses due to bodily injury. One approach is the “lost earnings approach”. This approach attempts to directly measure the decrease in the plaintiff’s future earning level by projecting...

Personal Injury Damages and Taxation

A couple of weeks back I posted on the issue of damages and taxation. The discussion was focused on awards in respect of lost profits. Someone asked me whether the same concepts apply to personal injury damages? The short answer...

Inflation and Family Law

I was looking through my oldest daughter’s baby book last night and found that we had noted the price of gas at $0.70 per litre; I had noted at the time that this was “really high”! This got me thinking...

Dunkin’ Donuts c. Bertico inc., Part II: Lost Profit & Loss of Business Value

Towards the end of its decision in Dunkin’ Brands Canada Ltd. c. Bertico inc.2015 QCCA 624, the Quebec Court of Appeal discussed the issue of whether an award for both a) lost profits up to 2005 and b) loss of business...

Untying the Knot: A Forensic Accountant’s View of Divorce Proceedings

During the course of matrimonial disputes, there are often situations where solicitors find it helpful to engage specialist investigators and appraisers. In particular, forensic accountants can help to provide the court with a clearer view of the true financial position...

Accountants and Conflicts of Interest

In the legal and accounting professions, potential conflicts of interest can arise before or during the course of an engagement. Most firms have policies and procedures in place that govern how conflicts are identified and managed, to ensure that client...

Rescission under the Ontario Arthur Wishart Act: Quantifying the Remedy

It has now been thirteen years since the Ontario Arthur Wishart (Franchise Disclosure) Act, 2000, SO 2000 [1], was enacted. The Act, named after Arthur Wishart, a Conservative MPP who championed the rights of franchisees in the 1970's and 1980's,...

Accounting For Attorneys

It is becoming increasingly important for attorneys to understand financial statements and their relevance to various types of business and legal situations. The non-accountant attorney will greatly benefit from a basic understanding of the key principles of accounting. Equally important...

Economic and Industry Conditions: Considerations and Tools for Disability Claim Assessment

In recent years the news headlines have been filled with stories about the global financial crisis. Fears of a double-dip recession, the ongoing U.S. and European debt crisis, mortgage foreclosures and lingering high unemployment are issues that continue to dominate...

Astronomy or Astronomical: Did the Mayans project the future?

Much like predictions based on interpreting the Mayan Calendar, determining the career path of a child or a student is always a difficult exercise. Typically, with an individual who has already commenced their work-life, a history of employment would be...

Calculating Income Loss

Assessing the income lost by a personal injury victim depends on whether the casualty is self employed, in which case assessing the loss becomes a lot more complicated. An expert on insurance litigation for MDD Forensic Accountants gives some guidance....

Clarifying Financial Remedies Under the Arthur Wishart Act

It is almost ten years since the Arthur Wishart (Franchise Disclosure) Act was introduced in Ontario. The Act seeks to protect often unsophisticated purchasers of franchise rights by requiring that certain disclosures be made to franchisees prior to entering into...

Backing out of a Franchise Just Got Easier

Section 6(6) of the Arthur Wishart Act gives franchisees the right to rescind their franchise agreements in the event that they do not receive a disclosure document. Ostensibly, the rescission remedy is designed to return the franchisee to the position...

Forensic Accountants Make It Add Up

Corporate fraud, insider trading, 9/11, intellectual property infringement the list goes on as to instances where parties have committed acts resulting in financial losses. The legal challenge in proving financial wrongdoing is a minefield in itself, but what steps need...

Fight the Battle on Two Fronts – Liability and Damages

Plaintiff and Defense attorneys are guilty! Guilty of waiting until the last minute to address areas of damages. MDD is very often retained in litigation engagements when the measurement of damages takes a back seat to liability and causation. Although...

The Role of a Forensic Accountant as an Expert Consultant and an Expert Witness

For many years, attorneys on both sides of the courtroom have turned to forensic experts to support their position as well as to identify the potential strengths and weaknesses in the arguments of opposing counsel. Additionally, attorneys can use expert...

Business Valuations: When You Would Need One

Business valuations in one form or another have been around for decades. As a result of the Eighteenth Amendment to the United States Constitution, the Internal Revenue Service began issuing memorandums and directives relating to methods for determining values and...