Valuing a Franchise System

05 July, 2018

05 July, 2018 Ephraim Stulberg

Ephraim Stulberg Canada

Canada

Valuing a franchise system, or “franchisor”, is in many ways very similar to the valuation of any other type of business; it is a function of the forecasted levels of cash flows that the business will generate, and the risk associated with those cash flows. Yet there are some particular factors that make valuing franchisors very tricky. This brief article touches on some of them.

Franchisors – Who are they?

The first point we need to clarify is what we mean when we speak of “franchisors”. Broadly speaking, a franchisor is a business that earns its income by granting the privilege to one or more franchisees to do business and offers some form of ongoing assistance and oversight in return for ongoing monetary consideration.

Franchisors operate in a variety of industries. The largest industry sector is in the food services; these businesses made up around 40% of the membership in the Canadian Franchise Association in 2017.[1] Tim Hortons’, McDonalds, Swiss Chalet – you get the picture. But there are many other types of franchisors in the retail and service industries. Most hotel chains are franchised, as are most automobile dealerships and the guys who promise to remove junk from your house at all hours of the day. These different industries obviously have different valuation characteristics.

There are also different types of business structures for franchisors. Thus:

- Some franchisors are what one might call “pure plays” (i.e. their income derives almost solely from the sale of franchises and the receipt of royalties). On example of this type of franchisor is Dine Brands Global Inc., the franchisor for the “Applebee’s” and “IHOP”.

- Other franchisors have structured their publicly traded shares as “royalty income funds”, which receive a portion of the royalties from the franchisees, while many of the expenses of operating the system are incurred in a separate company. Examples include Keg Royalties Income Fund and Boston Pizza Royalties Income Fund.

- Still other franchisor companies are hybrids, with a significant chunk of their revenue (though not necessarily their profit) coming from corporate-owned stores or from the sale of inventory to franchisees.

In a similar vein, while some franchisors hold a lot of real estate (e.g. McDonalds, Canadian Tire (until recently)), others do not.

What this means is that it is very important to understand the business of the franchisor you are valuing. It may hold several different sources of value: a stream of royalties, one or more actual operating businesses, and real estate. In order to gain a true grasp of the value of the business, you need to disaggregate and understand the different sources of value.

Valuation Approaches

There are three main approaches to valuing a business or asset: the income approach, market approach and asset approach. Of these, only the first two have any real relevance to valuing franchisors.[2] Stated very briefly:

- Under the income approach, the business valuator quantifies the present value of future cash flows associated with share ownership. The calculated future cash flows are discounted at a rate of return appropriate for the risks associated with those cash flows.

- Under the market approach, the business valuator determines the fair market value of the company based on comparable public companies and/or transactions involving comparable companies.

Income Approach

The three main drivers of value under the income approach are a) the current level of cash flows, b) projected growth and associated reinvestment, and c) risk. Let’s take a look at each one.

Cash Flows

For “pure play” franchisors, this issue can be relatively simple. Operating margins for franchisors are generally high; there is also typically fairly little in the way of capital expenditures. Furthermore, franchisors as a whole tend to carry fairly little debt relative to their equity values (unless they have made acquisitions). They also tend to carry fairly low working capital balances. All of this means that in general, after-tax net income can serve as a reasonable proxy for cash flows.

For franchisors who also earn revenue from other sources (e.g. sale of inventory, operation of corporate stores), the analysis can become more complicated, and it will be necessary to consider things like capital expenditures to upgrade stores, changes in minimum wage legislation and commodity prices, and all of the other complicating factors that go into valuations of businesses in other industries.

Growth

For franchisors, growth can come from two main sources: a) growth in the number of franchisees and b) growth in income per franchisee. In addition, growth can also come from acquisitions.

Growth in the number of franchisees can lead to multiple sources of revenue growth. In additional to new royalty streams, franchisors also typically charge an initial franchise fee that is payable upfront; this can often be substantial and can be a significant source of revenue. Some franchisors also serve as suppliers to their franchisees and earn income from markups on the supplies they sell. Franchisors can also assist their new franchisees manage the build-out of their locations, charging a management fee.

In many businesses, growth is accompanied by significant cash outflows as companies are required to carry additional inventory, carry more accounts receivable and build larger facilities. Franchisors do not have to deal with these issues to nearly the same degree.

That said, franchisors face other issues when it comes to growth. There is a cost associated with finding new franchisees in new territories, and for that reason many franchisors outsource that function to master franchisees. The master franchisee will assist the franchisor in developing franchisees in a given territory, but only in exchange for a significant cut of the new franchisees’ franchise fees and royalties.

Moreover, growth within a territory can result in friction with existing franchisees. The addition of a new location within proximity to a franchisee can lead to great overall system sales (and thus more royalties and other payments to the franchisor); but this comes at a cost to the existing franchisee, who in some sense becomes a competitor to the newcomer and will likely see a reduction in income. If the reduction is too great, the existing franchisee may go out of business.

Risk

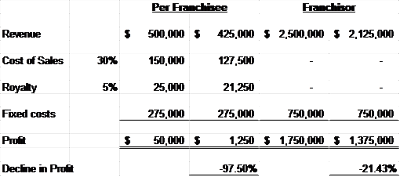

Established franchisors are relatively immune from macro-level trends. To understand why this is the case, consider the difference between a franchisor and a franchisee of a restaurant chain. Assume that each of a chain’s 100 franchisees earns an average of $500,000 in revenue per year, that the costs of sales equals 30% of sales, the royalty is 5%, and fixed costs (labour, rent, utilities) equals 55% of sales, giving it a profit margin of 10%, or $50,000 per year. The franchisor makes $25,000 in royalties (5% of $500,000) per franchisee, and $2.5M overall from the 100 franchisees.

If the market shifts and the franchisees sales decline by 15%, the franchisor’s profit from the restaurant will also drop by around 21%;[3] however, the franchisees’ profits will drop by almost 98%.

The fact that a franchisor’s profits are less subject to large swings based on small changes in revenue is an advantage and lowers the riskiness of an investment in a franchisor.

On the other hand, there are also risk factors that are significantly higher for franchisors than for other businesses. Many of these are legal in nature. Franchisors can be susceptible to class actions of various types, although the success rate for these so far in Canada has been poor.[4]Franchisors are also subject to a rigorous disclosure regime in many Canadian provinces; the failure to provide a proper Franchise Disclosure Document (“FDD”) can be severe, with franchisees potentially eligible to rescind their agreements and recover all of their costs and losses within the first two years of signing the franchise agreement. In my experience dealing with quantifying such claims, the average bill to a franchisor is somewhere in the $300,000 to $500,000 range, plus legal costs.

Market Approach

As we discussed above, franchise systems derive their value from many different sources. That can make the market approach difficult to apply; it is difficult to speak of a standard valuation multiple based on revenue in the franchising industry. Thus:

While royalty income funds (e.g. Boston Pizza Royalties Income Fund, Keg Royalties Income Fund) have tended to trade at multiples of over 10 times revenue, other hybrid franchisor public companies (e.g. Imvescor Restaurant Group Inc.) have traded at around five times revenue. Multiples of revenue are therefore generally not a good approach to use.

As described above, franchisors who derive most of their revenue from franchising (as opposed to corporate stores) generally are less subject to volatile changes in their profits. Royalty income funds are even less volatile, since their costs are minimal.

Differences in growth rates can also affect multipliers; firms that are expected to grow rapidly will attract higher multipliers.

In summary, the market approach is a difficult approach to apply for franchisors.

Conclusion

Conceptually, valuing a franchise system is in many ways no different than valuing any other business: it requires an understanding of the industry and the business, and the assessment of cash flows and risk. Executing on these concepts can pose a challenge.

By Ephraim Stulberg.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

2018 CFA Accomplishment Report

The asset approach is generally one that is more applicable to companies whose main value derives from their individual asset holdings (e.g. real estate holding companies).

I have assumed a level of fixed costs for the franchisor similar to Dine Equity, a “pure play” franchisor.

Several notable examples include:

- Fairview Donut Inc. v. The TDL Group Corp., 2012 ONSC 1252 (brought by Tim Horton’s franchisees over the introduction of a breakfast menu). Certification denied.

- 1250264 Ontario Inc. v. Pet Valu Canada Inc., 2016 ONCA 24 (brought by Pet Valu franchisees over the alleged failure of the franchisor to share volume rebates with franchisees). Certification denied.

- 2038724 Ontario Ltd. v. Quizno’s Canada Restaurant Corporation, 2014 ONSC 5812 (brought by Quizno’s franchisees over allegations of price fixing). Certification granted, but later settled for a small amount.

Ephraim Stulberg

B.A, M.A, M.BA, CPA, CA, CBV, CFF, Partner/Senior Vice President

- +1 416.366.4968

- estulberg@mdd.com

- Toronto, ON, Canada

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

ESG Disputes and Business Valuation

Environmental, Social and Governance (“ESG”) factors have gained increasing importance in recent years as society has become more aware of how corporate conduct affects stakeholders, the environment and humanity at large. From issues such as climate change to socially responsible...

Business Valuation, Growth Rates and Climate Change: a Case Study of Vail Resorts

This past summer’s heatwaves and wildfires served for many as alarming reminders of climate change. Hotter summers, colder winters, and more hurricanes are amongst the symptoms of a changing global climate[1]. These climatic effects will impact different businesses in different...

COVID-19’s Impact On Business Valuation

This is the second blog post co-authored by MDW Law Partner, Christine Doucet, and MDD Forensic Accountants Partner, Jarrett Reaume, addressing various aspects of COVID-19’s impact on business owners and family law issues. Their first blog post was “Guideline Income...

Is Kylie Jenner a Billionaire, or Even Close? Part III

I hope this will be the final installment in this series, but one never knows. Back in the summer of 2018, I wrote a short piece questioning a sensational Forbes magazine article claiming that Kylie Jenner was worth $1B, based mainly...

Is Kylie Jenner a Billionaire, or Even Close? Part II

A little over a year ago, I wrote a short blog post taking issue with a Forbes magazine article that had concluded that Kylie Jenner's net worth was around $900 million. In light of last week’s news that Coty Inc., a publicly traded cosmetics firm, is...

Buying Shares in an NFL Player? Business Valuation Principles Still Apply

In my last post, I argued that an investor in Kylie Jenner’s cosmetics company was essentially investing in Ms. Jenner’s personal brand, and that the earnings stream for that brand was of a finite life. The post got me thinking:...

Is Kylie Jenner Really a Billionaire, Or Even Close?

A few weeks ago, Forbes created a social media storm when it proclaimed that Kylie Jenner was poised to become the world’s youngest self-made billionaire. Many thumbs were worn out debating the appropriateness of the term “self-made”, and apparently a GoFundMe page...

Valuing a Franchise System

Valuing a franchise system, or “franchisor”, is in many ways very similar to the valuation of any other type of business; it is a function of the forecasted levels of cash flows that the business will generate, and the risk...

How Much Is Your Business Worth?

As a Chartered Business Valuator (CBV), almost every business owner I meet wants to know the answer to this question: “How much is my business worth?” There can be many reasons for asking this question: they may be planning to...

What Type of Business Valuation Do I Need?

In my previous article, I discussed the critical need for business owners to have their business valued by a professional appraiser. In this article I will discuss the two types of business appraisals that you might want to consider. Calculation...

Should I Have My Business Valued?

What's so important about having a valuation of my company? Small business owners spend most of their time IN THEIR business and not ON THEIR business. Further, they view expending money on getting a professional valuation performed as a completely...

Business Valuations & Why It Pays To Use Genuine Experts

The Basics Assets have value if they will give rise to future economic benefits. For businesses, these future economic benefits take the form of either the expected net income stream or the amount that could be realised in the short...

Gift Cards and the Illiquidity Discount – A Valuation Perspective

With the busiest season of the year for retail sales upon us, you are no doubt wondering what to buy for that special someone. If you’re reading this blog – and I have every reason to believe you are –...

I Lost My Customers and It’s Your Fault!

In Schwartz Levitsky Feldman LLP v. Werbin, 2015, an action was put forward by Schwartz Levitsky Feldman (SLF) claiming loss of profits due to the departure of Mr. Werbin. The firm contended that they purchased Werbin’s clients when they purchased...

The Dividend Double Count

In this post, I touch on a common error I encounter in dealing with a financial analysis of multiple companies owned by the same group or individual. I call this error the “dividend double count”, for reasons that will become...

Adding up the Damage: Lost Profits vs. Business Value

When a business is destroyed as a result of wrongdoing, there are two commonly used methods by which the plaintiff’s damages may be measured. One method is to appraise the value of the plaintiff’s business at the date of loss;...

Calculated Risk: A $75M Award Adds Urgency to Pre-Judgment Interest Considerations

Pre-judgment interest is often the last thing litigants ponder. A recent award of $75 million in pre-judgment interest in Eli Lilly v. Apotex, 2014 FC 1254 (“Cefaclor”) may change that. Cefaclor involved the infringement of patents for an antibiotic. Damages...

Personal Injury Losses and the Self-employed: A Business Valuation Perspective on Labour & Capital

Business valuation concepts can be critical for the proper quantification of personal injury damages, particularly in the context of self-employed individuals. Business valuators are commonly called upon to assess the fair market value of small, owner-managed businesses. One of the...

5 Ways You Should Be Using Your Financial Expert

Moore v. Getahun 2015 ONCA 55 is a case that has already generated a lot of discussion and navel gazing in both the legal and expert communities, and I hesitated for quite a while before deciding that I had anything worthwhile to...

Financial Statements, Disclosure and the Arthur Wishart Act

The topic of what types of financial statements must be included in a disclosure document in order to comply with the disclosure requirements of the Arthur Wishart Act (“AWA”) was discussed at a recent dinner put on by the OBA’s Franchise Law section....

Dunkin’ Donuts c. Bertico inc., Part II: Lost Profit & Loss of Business Value

Towards the end of its decision in Dunkin’ Brands Canada Ltd. c. Bertico inc.2015 QCCA 624, the Quebec Court of Appeal discussed the issue of whether an award for both a) lost profits up to 2005 and b) loss of business...

Dunkin’ Donuts c. Berticoinc, Part I: The Benchmark Approach to Lost Profits

In April 2015, the Quebec Court of Appeal released its decision in Dunkin’ Brands Canada Ltd. c. Bertico inc. 2015 QCCA 624. The Court of Appeal upheld the trial judge’s ruling (Bertico inc. c. Dunkin' Brands Canada Ltd., 2012 QCCS 2809) that...

Untying the Knot: A Forensic Accountant’s View of Divorce Proceedings

During the course of matrimonial disputes, there are often situations where solicitors find it helpful to engage specialist investigators and appraisers. In particular, forensic accountants can help to provide the court with a clearer view of the true financial position...

Rescission under the Ontario Arthur Wishart Act: Quantifying the Remedy

It has now been thirteen years since the Ontario Arthur Wishart (Franchise Disclosure) Act, 2000, SO 2000 [1], was enacted. The Act, named after Arthur Wishart, a Conservative MPP who championed the rights of franchisees in the 1970's and 1980's,...

Proving Rescission Damages under the Provincial Franchise Acts

In October 2012, the Manitoba Franchise Act was proclaimed into law. The legislation, like its counterparts in several other provinces (including Ontario’s Arthur Wishart Act), provides franchisees with the right to rescind a franchise agreement within two years if a...

Accounting For Attorneys

It is becoming increasingly important for attorneys to understand financial statements and their relevance to various types of business and legal situations. The non-accountant attorney will greatly benefit from a basic understanding of the key principles of accounting. Equally important...

Clarifying Financial Remedies Under the Arthur Wishart Act

It is almost ten years since the Arthur Wishart (Franchise Disclosure) Act was introduced in Ontario. The Act seeks to protect often unsophisticated purchasers of franchise rights by requiring that certain disclosures be made to franchisees prior to entering into...

Backing out of a Franchise Just Got Easier

Section 6(6) of the Arthur Wishart Act gives franchisees the right to rescind their franchise agreements in the event that they do not receive a disclosure document. Ostensibly, the rescission remedy is designed to return the franchisee to the position...

Fight the Battle on Two Fronts – Liability and Damages

Plaintiff and Defense attorneys are guilty! Guilty of waiting until the last minute to address areas of damages. MDD is very often retained in litigation engagements when the measurement of damages takes a back seat to liability and causation. Although...

The Role of a Forensic Accountant as an Expert Consultant and an Expert Witness

For many years, attorneys on both sides of the courtroom have turned to forensic experts to support their position as well as to identify the potential strengths and weaknesses in the arguments of opposing counsel. Additionally, attorneys can use expert...

Business Valuations: When You Would Need One

Business valuations in one form or another have been around for decades. As a result of the Eighteenth Amendment to the United States Constitution, the Internal Revenue Service began issuing memorandums and directives relating to methods for determining values and...

Financial Remedies Under the Arthur Wishart Act

It is almost ten years since the Arthur Wishart (Franchise Disclosure) Act was introduced in Ontario. The Act seeks to protect often unsophisticated purchasers of franchise rights by requiring that certain disclosures be made to franchisees prior to entering into...